Healthcare is entering a new phase of innovation, driven by technologies that are changing how diseases are detected, treated, and managed. From artificial intelligence that assists clinicians in making faster diagnoses to advanced biotechnology enabling personalized treatments, the pace of transformation is accelerating across the healthcare ecosystem.

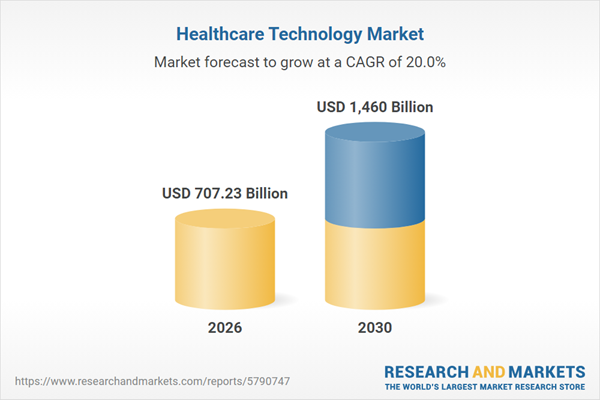

The global healthcare technology market is projected to reach $1.46 trillion by 2030, driven by AI-supported care, cloud-based systems, remote monitoring, digital diagnostics, and virtual care becoming standard rather than experimental.

These technologies are not only improving patient outcomes but also helping healthcare providers address growing challenges such as rising costs, workforce shortages, and increasing demand for care. As investments in digital health, medical devices, and life sciences continue to grow, organizations that understand and adopt these innovations will be better positioned to deliver more efficient, accessible, and patient-centered healthcare.

This article explores 10 emerging healthcare technologies that are shaping the future of medicine and redefining the standards of care worldwide.

1. AI Diagnostics

AI-powered diagnostics is becoming one of the most important shifts in medicine. These tools can review X-rays, MRIs, CT scans, ultrasounds, DXAs, and other medical images to help doctors detect disease faster and more accurately.

The technology is already being used across cancer, heart disease, brain and neurological conditions, lung disorders, and obstetrics. In many of these areas, AI helps identify patterns that may be difficult to catch during a busy clinical workflow.

The market growth shows how quickly adoption is rising. This growth is being driven by rising imaging volumes, a shortage of skilled radiologists, the need for earlier disease detection, and wider use of healthcare data.

A real-world example shows why this matters. In a BBC-reported NHS trial, an AI tool called Mia reviewed mammogram scans alongside clinicians and helped detect tiny signs of breast cancer in 11 women that had not been picked up by doctors. This does not mean AI is replacing clinicians. It shows how AI can act as an extra safety layer, helping doctors catch early warning signs sooner.

More than 6,000 patents are focused on AI-driven image analysis alone, making it one of the most active IP areas in digital medicine. The fastest-growing patent categories include pattern recognition for image-based diagnosis, identification of new physiological patterns, treatment response monitoring, and clinical workflow management.

Early disease detection is also emerging as a rapidly growing patent area, showing that companies are not only building diagnostic tools but also protecting the methods behind faster and earlier disease discovery.

The next phase will be about practical adoption. AI diagnostics will need to fit smoothly into hospital workflows, support human review, and prove that it improves patient outcomes. With companies filing heavily around image analysis, diagnostic automation, and AI-assisted decision support, this area is likely to remain one of the most important medicine innovation spaces in 2026.

2. CRISPR Gene Editing

CRISPR and gene editing therapies are moving from long-term promise to real clinical use. For years, CRISPR was seen as a technology that was always “almost ready.”

That changed in 2023, when CASGEVY became the first CRISPR-Cas9 therapy approved for sickle cell disease and transfusion-dependent beta-thalassemia. This approval showed that gene editing is no longer limited to research labs. It is becoming a real therapeutic category.

Recent developments also show how fast the field is advancing. In 2025, a personalized in vivo CRISPR therapy was designed and delivered to a single infant within six months, setting an important example for rapid treatment development. Stanford also introduced CRISPR-GPT, an AI-supported tool that can help design CRISPR experiments much faster, reducing the time needed to move from an idea to a testable therapy.

In 2026, several areas are worth watching closely. CRISPR Therapeutics is testing approaches targeting Lp(a), a cardiovascular risk marker, with early-stage reductions of up to 73% reported.

Scribe Therapeutics is preparing a trial targeting PCSK9, a gene linked to cholesterol control, using an epigenetic silencing platform. Prime Medicine is also moving toward trials for Alpha-1 antitrypsin deficiency. In China, Correctseq Therapeutics has advanced one of the first base-editing therapies delivered through lipid nanoparticles into human dosing.

CRISPR is one of the most closely watched IP areas in biotech, with rights covering editing methods, delivery systems, guide RNA design, cell modification workflows, and clinical applications.

The commercial side is now becoming clearer as well. CASGEVY generated $116 million in full-year 2025 revenue, with patient initiations nearly tripling year over year. This is an important signal because it shows CRISPR is no longer just a scientific platform. It is becoming a commercial medicine category.

The next challenge will be safety, delivery, and immune response. One concern is immunogenicity, where the body’s immune system may recognize and react against the Cas9 protein. This could affect treatment safety or effectiveness. As a result, immune evasion strategies, safer delivery systems, and more precise editing tools are becoming major areas of research and patent filing.

In 2026, CRISPR will be one of the most important medicine innovations to watch because it is now crossing three key milestones at once: clinical validation, commercial adoption, and intense patent activity.

3. GLP-1 Drugs

GLP-1 medicines are no longer just diabetes drugs. What started with treatments like Ozempic for type 2 diabetes has now expanded into obesity, cardiovascular disease, kidney disease, sleep apnea, and even research around addictive behaviors. This wider impact is why many researchers are now calling this the beginning of “incretin era 2.0.”

A Mass General Brigham study published in Nature Medicine found that semaglutide reduced the risk of stroke and heart attack by 18% compared with another diabetes drug. Tirzepatide also lowered the combined risk of stroke, heart attack, and death by 13%. These findings show that GLP-1-based therapies may play a much larger role in chronic disease management than originally expected.

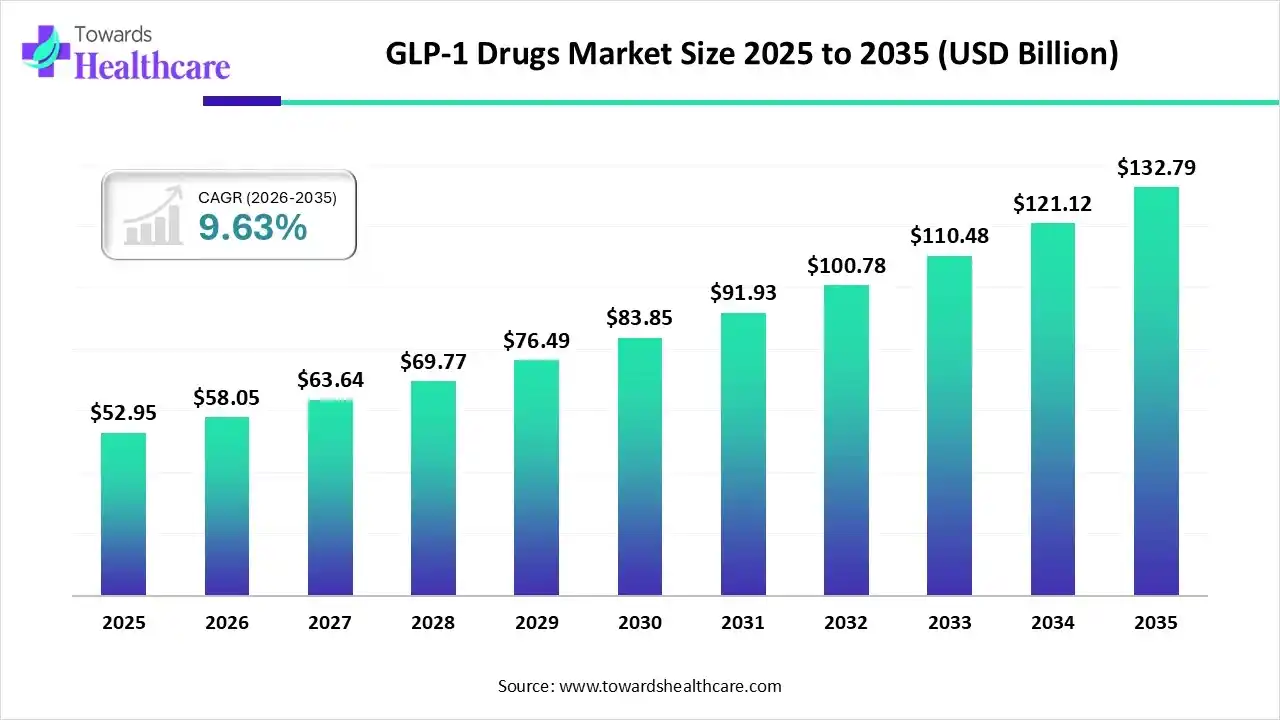

The global GLP-1 drugs market size began at US$ 52.95 billion in 2025 and is forecast to rise to US$ 58.05 billion by 2026. By the end of 2035, it is expected to surpass US$ 132.79 billion, growing steadily at a CAGR of 9.63%.

This growth is being driven by rising obesity rates, strong clinical outcomes, broader disease applications, and demand for more convenient treatment formats.

CagriSema, a combination of semaglutide and cagrilintide, showed strong results in the REDEFINE-1 trial, where 60% of participants lost at least 20% of their body weight.

Retatrutide, a triple GIP, GLP-1, and glucagon agonist, has shown some of the highest weight-loss results seen in this drug class so far. Eli Lilly’s orforglipron is also important because it is an oral GLP-1, which could make treatment easier for patients who prefer pills over injections. Tirzepatide is also being tested in Phase 3 trials for ulcerative colitis and Crohn’s disease, showing how the category is expanding beyond metabolic disorders.

Novo Nordisk has filed 320 US patent applications for semaglutide, with 154 granted. Follow-on patents could extend protection up to 2042, covering not only the drug itself but also formulations, dosing methods, and delivery systems.

For tirzepatide, Eli Lilly’s patent protection is expected to run until around 2036. Across the category, brand-name GLP-1 drugs hold an average of 19.5 patents per medicine, with many focused on delivery devices rather than the active ingredient.

The next phase of GLP-1 innovation will not only be about stronger weight loss. It will also be about broader disease coverage, easier delivery, patent battles, and affordability. In 2026, GLP-1 medicines are likely to remain one of the most watched areas in medicine because they sit at the center of clinical, commercial, and access debates.

4. CAR-T Cell Therapy

CAR-T therapy is becoming one of the most important advances in cancer treatment. In this approach, a patient’s immune cells are engineered to recognize and attack cancer cells, then infused back into the body.

It started mainly as a last-resort option for certain blood cancers, but in 2026, the field is moving toward earlier use, harder-to-treat cancers, and more scalable treatment models.

Recent clinical data shows why this area is gaining attention. In March 2026, a CAR-T therapy developed by Washington University School of Medicine, called sofi-cel or WU-CART-007, received FDA Breakthrough Therapy Designation for T-cell acute lymphoblastic leukemia and T-cell lymphoblastic lymphoma. These cancers are difficult to treat after relapse, with median survival often around six months.

In an international Phase 1/2 trial across the US, Australia, and Europe, WU-CART-007 achieved a 91% overall response rate and a 72.7% complete remission rate in evaluable patients. This was especially important because T-cell cancers are hard to treat with CAR-T.

The engineered cells can sometimes attack each other, a problem known as fratricide. The WU-CART-007 team addressed this through CRISPR engineering, making the therapy a strong example of how gene editing and cell therapy are starting to work together.

Another signal of where the field is heading came from the CAR-PRISM trial, presented at the 2026 American Association for Cancer Research annual meeting. The trial reported rapid and sustained measurable residual disease responses in high-risk smoldering myeloma patients, with no progression events. This suggests CAR-T may move earlier in the cancer treatment timeline, rather than being used only after other options fail.

The IP landscape covers cell engineering methods, antigen targets such as CD19, CD7, CD22, and BCMA, manufacturing processes, and delivery mechanisms. Approved CAR-T therapies already include Kymriah, Yescarta, Tecartus, Breyanzi, Abecma, Carvykti, and NexCAR19, showing how quickly the category has expanded from research into commercial medicine.

One of the biggest patent and R&D themes is allogeneic, or “off-the-shelf,” CAR-T therapy. Unlike today’s personalized CAR-T treatments, which require immune cells to be collected and engineered for each patient, allogeneic CAR-T could use pre-made standardized cells. Companies such as Fate Therapeutics, Cellectis, and BlueRock Therapeutics are active in this area.

This matters because manufacturing is still one of the biggest bottlenecks in CAR-T therapy. Personalized production can take weeks, and many patients do not have that time. If off-the-shelf CAR-T becomes safe and effective, it could make cell therapy faster, more accessible, and easier to scale.

In 2026, next-generation CAR-T therapies are worth watching because the field is moving on three fronts at once: treating tougher cancers, entering earlier stages of disease, and solving the manufacturing barriers that have limited access so far.

5. Next-Generation Wearable Health Monitors

SLATE analysis shows that wearable health monitoring has moved through four development phases between 2011 and 2025 foundational sensing, rapid buildout, pandemic-driven acceleration, and the current commercialization and consolidation phase. The defining characteristic of this current phase is the shift from consumer wellness to clinical utility, and from cloud-dependent analysis to AI-driven edge computing where the device itself processes and flags health signals in real time.

The clinical focus in 2026 is on heart rhythms, blood oxygen, stress biomarkers, and glucose moving well beyond step counts and sleep tracking into data that can meaningfully guide healthcare decisions. Glucose monitoring illustrates where the technology is heading.

Patent activity is developing across four clusters: subcutaneous continuous glucose monitors, non-invasive optical sensing, sweat and tear-based biofluid platforms, and AI-driven predictive analytics. Dexcom has filed multiple machine-learning-based glucose prediction patents in Japan between 2023 and 2025, focusing on forecasting glucose changes rather than simply measuring them.

The competitive landscape is also broadening. Patent activity from companies like Analog Devices, Koninklijke Philips, and Starkey Laboratories signals that semiconductor, medtech, and hearing technology players are entering wearable health monitoring not just traditional wearable brands. Micro Tech Medical Hangzhou’s 2023 European patent for a cloud-based CGM correction system using big data reflects the broader direction: wearables becoming connected diagnostic platforms combining sensors, AI models, cloud systems, and clinical decision support.

The remaining barrier is clinical trust. Clearer regulatory and clinical guidelines are needed on when wearable-detected signals should trigger medical action particularly around drug treatment decisions or emergency escalation. R&D teams tracking this space should watch for regulatory movement on wearable data standards as closely as they watch the hardware and AI developments.

6. Regenerative Medicine and Stem Cell Therapy

Stem cell research has been building momentum for decades, and in 2026 it is starting to reach more patients through real clinical programs. The field is moving beyond early lab promise into treatments designed to repair damaged tissues, replace lost cells, and slow disease progression in conditions where current options are limited.

The market and clinical progress show how far the field has come. Stem cell therapy and regenerative medicine is now being described as a $28 billion clinical reality. Key programs include Phase II/III trials using iPSC-derived cardiomyocytes for heart failure and iPSC-derived dopaminergic neurons for Parkinson’s disease, both of which have reported promising interim results.

One important clinical signal came from a Phase II randomized controlled trial published in The Lancet. The study showed statistically significant slowing of motor function decline in ALS patients treated with intrathecal neural stem cell injections. This matters because ALS remains one of the hardest diseases to treat, with very few options that can slow progression.

A 2025 landscape analysis reported 115 regulatory-approved clinical trials testing 83 human pluripotent stem cell-derived products. More than 1,200 patients had already been dosed, with no generalized safety concerns identified. This does not remove the need for long-term monitoring, but it shows that the field is gaining stronger clinical confidence.

Another major milestone is the move toward off-the-shelf stem cell therapies. XcellSmart Biopharmaceutical initiated the world’s first allogeneic iPSC-derived spinal neural progenitor cell therapy trial for spinal cord injury. The trial was approved by both China’s NMPA and the US FDA, making it an important example of how standardized cell therapies may become easier to scale.

A major shift in 2025 and 2026 is also happening around MSC-derived exosomes. These are tiny vesicles released by stem cells that carry therapeutic materials such as miRNAs and growth factors. They are being explored as an alternative to whole-cell transplantation, which has often faced problems such as poor cell survival after injection. Exosomes may offer a more stable and controllable way to deliver regenerative signals.

Heavily patented areas include iPSC reprogramming methods, automated bioreactor systems, cell engineering workflows, and differentiation protocols. Companies such as Fate Therapeutics, Cellectis, BlueRock Therapeutics, and REPROCELL are active in this space. REPROCELL’s July 2025 Type II Drug Master File submission to the FDA for GMP-compliant iPSC Seed Clones also shows how companies are preparing the manufacturing base needed for clinical-scale regenerative therapies.

Regulatory support is helping the field move faster. The FDA’s RMAT designation and Fast Track pathways are being used to accelerate promising regenerative medicine programs, especially where there is high unmet medical need.

In 2026, stem cell and regenerative medicine is worth watching because it is moving closer to practical use in diseases like heart failure, Parkinson’s disease, ALS, and spinal cord injury. The next challenge will be proving durable benefits, scaling manufacturing, and making these therapies safe and accessible beyond small trial populations.

7. De Novo Protein Design

This one doesn’t get the headlines it deserves. Scientists can now design proteins from scratch, engineering enzymes with functions that don’t exist anywhere in nature. This opens completely new doors in drug development, because instead of searching for molecules that already exist and repurposing them, researchers can build precisely what they need.

A September 2025 review published in Biology described how AI-driven de novo protein design is advancing through generative models, especially language models and diffusion models. These systems can create novel protein structures and functions much faster than traditional discovery methods.

One reason this is so important is the size of the protein design space. There are more possible protein sequences than researchers could ever test manually. AI helps search this space more efficiently and identify designs that nature may never have produced through evolution. State-of-the-art design protocols are now reaching experimental success rates close to 20%, which is a major step forward for such a complex field.

AlphaFold has also become a foundational tool for drug discovery. Developed by DeepMind, it predicts 3D protein structures from amino acid sequences, helping researchers understand how a designed protein may fold and behave. This makes it easier to create therapeutic proteins, binders, enzymes, and antibodies with more targeted functions.

The field is also moving toward more autonomous discovery. A 2025 Nature paper described a “virtual lab” of AI agents that designed new SARS-CoV-2 nanobodies, with the design process running largely on its own. This shows how AI could shorten the time needed to move from biological idea to testable molecule.

On the clinical side, companies such as Iambic and Generate Biosciences are expected to have multiple AI-designed drugs in clinical trials by 2026. These programs are targeting conditions such as ALS and autoimmune diseases, making 2026 an important year for testing whether AI-designed molecules can move from computational success to real patient benefit.

In 2026, AI-designed proteins are worth watching because they could change how new medicines are discovered. Instead of only searching nature for useful molecules, researchers can now design new biological tools for specific therapeutic purposes.

8. 3D Bioprinting

3D printing has already changed parts of medicine by making custom prosthetics, dental products, surgical guides, and patient-specific implants easier to produce.

The next frontier is bioprinting, where living cells are used like “ink” to build tissue-like structures. This could eventually help repair damaged tissues, create better disease models, and reduce reliance on animal testing in drug development.

The field is moving in stages. A 2025 roadmap paper published in Device outlined how medical 3D printing has evolved from basic prototypes to more advanced bioprinting systems. It identified three major clinical pathways: patient-specific implants, organ models for surgical planning, and tissue scaffolds seeded with patient-derived cells for regenerative medicine.

Patient-specific implants are already being used in clinical settings, especially where shape and fit matter. Organ models are also gaining traction because they help surgeons plan complex procedures before operating. Tissue scaffolds are still more research-focused, but they are important because they could support the growth of living tissue for repair and regeneration.

One promising area is tracheal tissue engineering. A 2026 paper in Frontiers in Cell and Developmental Biology discussed tracheal biofabrication as a frontier application, showing how researchers are working to print complex airway structures that may one day support repair or replacement.

A notable material breakthrough came from Northeastern University, where Professor Guohao Dai and collaborators patented a new elastic hydrogel for 3D printing soft living tissues. This matters because many current bioprinting materials harden as they cool. That may work for bone or rigid implants, but it is not suitable for tissues such as heart valves, blood vessels, or liver tissue, which need to stretch, bend, and recoil. Elastic hydrogels could help close this gap and support more realistic soft tissue printing.

Patent activity in bioprinting is expanding across several technical areas. Key patent categories include bioink formulations, printer hardware designs, cell culture methods, vascularization strategies, and specific organ or tissue architectures. Vascularization is especially important because printed tissues need blood vessel-like networks to stay alive and function properly.

The market is also expanding beyond prosthetics and implants. 3D-printed medical devices and bioprinted tissues are now being explored for surgical planning, regenerative medicine, and drug screening models. These applications may reach practical use earlier than fully transplantable printed organs.

In 2026, 3D bioprinting is worth watching because it is helping medicine move from replacement parts to living repair systems. Fully printed transplantable organs are still a longer-term goal, but the materials, printing methods, and patent base needed to get there are being built now.

9. Precision Medicine and Pharmacogenomics

Precision medicine is becoming more operationally practical in 2026. The approach using a patient’s genetics, lifestyle, environment, and disease biology to guide treatment has been a stated goal for years. Better genomic tools, stronger biomarker data, and growing clinical implementation programs are now making it actionable at scale.

Pharmacogenomics is the most clinically advanced component. A 2026 review in the Journal of Laboratory and Precision Medicine identifies it as essential to precision medicine genetic differences significantly affect how patients metabolize and respond to drugs. It is already guiding dosing for anticoagulants, chemotherapy agents, and psychiatric medications, reducing trial-and-error prescribing in routine clinical settings.

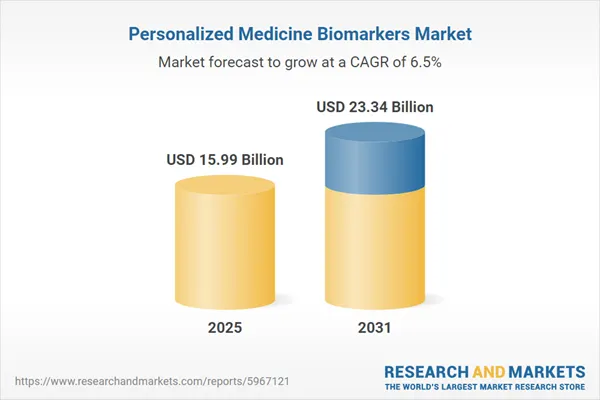

The market is also growing steadily. The global personalized medicine biomarkers market is projected to rise from $15.99 billion in 2025 to $23.34 billion by 2031. Pharmacogenomics holds the largest technology segment share at 30.2%, showing how central drug-response testing has become in the wider precision medicine space.

The next layer is multi-omics. Combining genomics, transcriptomics, proteomics, and metabolomics gives a more complete picture of patient biology and disease behavior than genomics alone. AI models integrating multi-omics data have achieved very high performance in drug response prediction, and companies are actively filing patents around algorithmic methods that interpret multi-gene interactions and predict treatment response.

Clinical implementation programs CPIC, the Dutch Pharmacogenomics Working Group, France’s PFMG2025, and the US eMERGE-PGx network are translating pharmacogenomic research into protocols that clinicians can use in practice. The European PREPARE trial is demonstrating how pre-emptive pharmacogenomic testing before prescribing can reduce adverse drug reactions at population scale.

For R&D teams, the patent focus areas to monitor are genetic marker diagnostic tests, custom dosage algorithms, and integrated systems combining genetic, environmental, and lifestyle data particularly where AI interpretation of multi-gene interactions is being protected.

10. Virtual Hospitals and AI-Augmented Telemedicine

Telemedicine grew quickly during the pandemic, but in 2026 it is becoming much more than a video call with a doctor. The next stage is virtual hospitals, where patients are monitored remotely through connected devices, AI tools, and specialist care teams. This model can support patients at home while still giving clinicians a continuous view of their health.

The main shift is from episodic care to continuous care. Instead of waiting for a scheduled appointment, virtual care platforms can track patient data in real time, flag possible risks, and connect patients with the right level of care. This is especially useful for chronic disease management, post-surgery recovery, elderly care, and patients who live far from specialist hospitals.

A 2026 University of Florida Medical Physiology overview shows how virtual consultations are now being used for acute conditions, skin problems, routine follow-ups, and long-term management of chronic diseases. This shows that telemedicine is no longer limited to basic consultations. It is becoming part of regular healthcare delivery.

AI virtual health assistants are also becoming more advanced. Earlier systems mostly handled simple questions or appointment support. Newer tools can take detailed medical histories, identify clinical red flags, support triage, guide follow-ups, and help route patients to the right care setting. This can reduce pressure on hospitals and help patients get faster direction when symptoms appear.

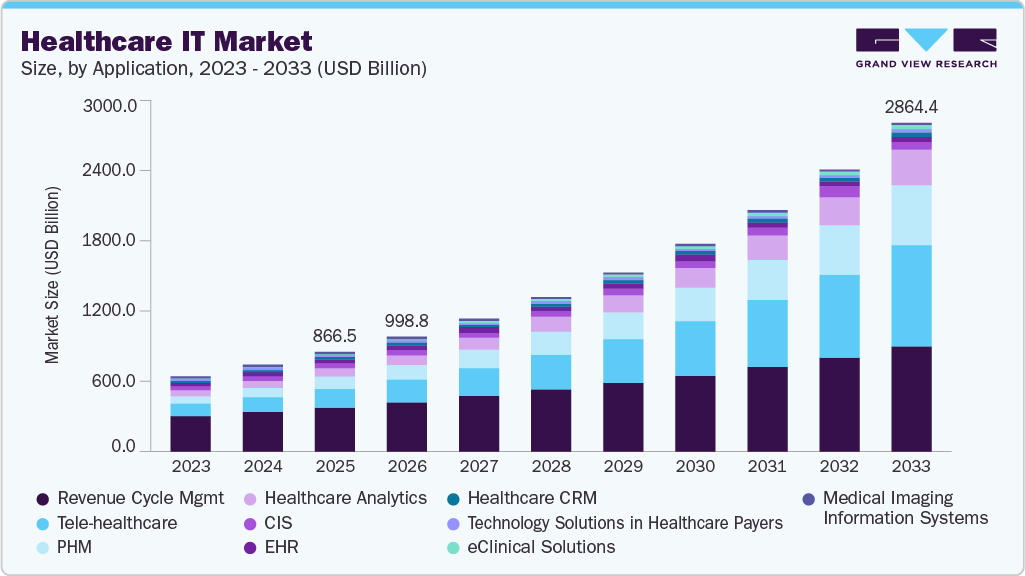

The market growth reflects this momentum. The AI healthcare IT market was valued at $866 billion in 2025 and is projected to reach $2.86 trillion by 2033, growing at a CAGR of 16.2%. Healthcare IT already holds a 21.5% share of the broader healthcare market, showing how deeply digital systems are becoming embedded in care delivery.

The regulatory landscape is also changing. The FDA’s January 2026 guidance update relaxed requirements for many clinical decision support tools. This could allow more AI tools that provide diagnostic suggestions or supportive clinical functions to reach clinics without full FDA review. While this may speed up adoption, it also raises concerns around bias, accuracy, patient safety, and accountability.

State-level oversight is beginning to take shape as well. Utah launched a first-in-the-nation pilot with Doctronic in early 2026 for autonomous AI patient consultations. At the same time, several US states have introduced bills requiring human oversight of AI-assisted clinical decisions. This shows that regulators are trying to balance faster innovation with clinical responsibility.

Patent and funding activity is also building around virtual care platforms, AI triage, remote monitoring, and digital clinical workflows. ARPA-H was expected to select innovation teams for next-generation virtual care platforms by June 2026, with competitive funding to follow. This could accelerate new models that combine wearable monitoring, AI-supported decision-making, and remote specialist access.

In 2026, virtual hospitals and AI-enabled telemedicine are worth watching because they could change where care happens. More patients may be treated, monitored, and guided from home, while hospitals focus on the cases that truly need in-person care. The next challenge will be proving clinical safety, protecting patient data, and ensuring that AI supports doctors rather than replacing human judgment.

How SLATE Helps Track Emerging Healthcare Technologies

This is where SLATE can help. Healthcare technologies are moving too quickly for teams to rely only on scattered news, research papers, patent databases, clinical trial updates, and market reports.

SLATE brings these signals together so R&D and innovation teams can see what is changing, where each technology is moving, and which companies are gaining momentum.

For example, in areas like wearable health monitors, SLATE can help track how the field has evolved over time, what patent clusters are emerging, which companies are filing actively, and where the technology is shifting from consumer wellness to clinical value. The same approach can be applied across AI diagnostics, CRISPR, CAR-T, GLP-1 drugs, regenerative therapies, precision medicine, 3D bioprinting, protein design, and virtual care.

Instead of only showing what has already happened, SLATE helps teams spot early signals: rising patent activity, clinical trial movement, company partnerships, technology gaps, regulatory shifts, and emerging application areas. That makes it easier to separate short-term hype from technologies with real technical and commercial potential.

In a year like 2026, that matters. The teams that can connect research, patents, market movement, and clinical adoption faster will be better placed to decide where to invest, partner, build, or compete next.