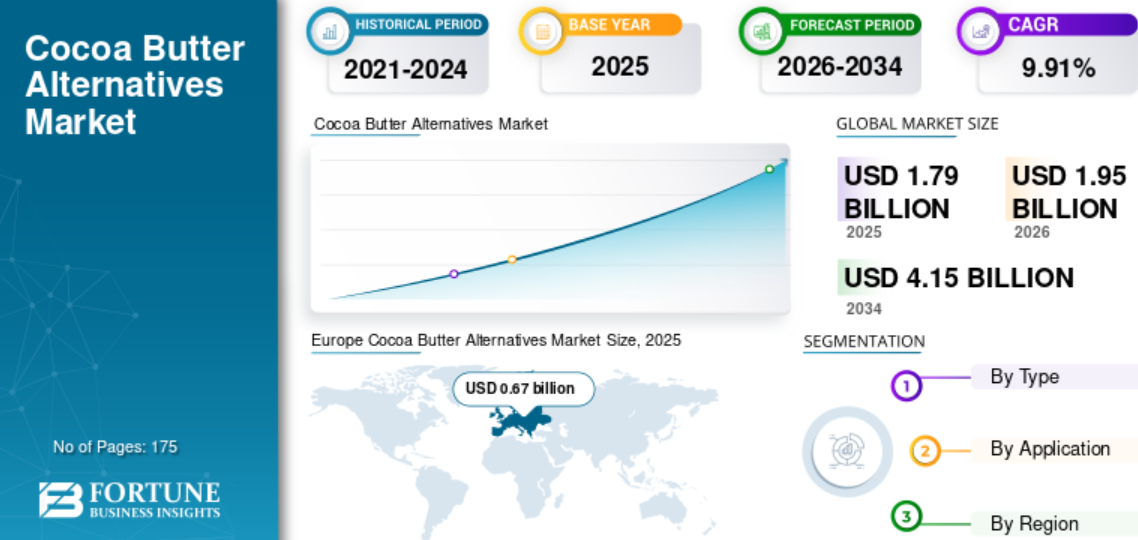

The cocoa butter alternatives market is no longer a quiet corner of the specialty fat industry. The global cocoa butter alternatives market size was valued at USD 1.79 billion in 2025 and projected to reach USD 4.15 billion by 2034 at a CAGR of 9.91%, it is becoming a fast-moving reformulation battleground and Europe, with a 37.27% market share, is where regulation, sourcing pressure, and product innovation are now colliding hardest.

At the center of this shift is palm oil. For years, conventional palm has been a practical feedstock for cocoa butter equivalents because it offers scale, functionality, and cost advantages. But under EUDR, it also brings deeper scrutiny, stronger traceability demands, and heavier documentation requirements.

For CBE manufacturers still dependent on conventional palm, the choice is becoming clear: build EUDR-ready supply chains quickly or move more aggressively toward palm-free alternatives.

The opportunity is strong, but the timeline is tight. Reformulation takes time. Companies need to test performance, secure supply, qualify suppliers, update documentation, and gain customer approval before new fat systems can move into commercial use. Those that start early will be better positioned to serve brands looking for clean-label, deforestation-free, and EUDR-ready ingredients.

Palm-free CBEs are no longer just an alternative ingredient choice. They are becoming a strategic readiness tool. The companies that move now can turn regulatory pressure, commodity volatility, and maturing alternative fat technologies into a market advantage before the window closes.

What is Cocoa Butter Equivalent?

A cocoa butter equivalent, or CBE is a speciality fat engineered to mimic cocoa butter’s unique triglyceride composition:

- Symmetric triglycerides like SOS (1,3-stearoyl-2-oleoylglycerol)

- POP (1,3-palmitoyl-2-oleoylglycerol)

- POS

This formulation gives cocoa butter its characteristic sharp melt at body temperature, snap at room temperature, and bloom resistance.

In the EU, chocolate makers can add vegetable fats other than cocoa butter within permitted limits, as long as the product is labelled properly. This makes CBEs useful for manufacturers that want to manage cocoa butter cost, improve product stability, and maintain the chocolate experience.

In pharmaceuticals, CBEs serve as suppository matrices, particularly in tropical markets where conventional cocoa butter struggles with heat stability. The cosmetics segment is projected to grow at the fastest rate of any CBE application category through 2032, driven by rising consumer demand for natural, traceable ingredients in personal care.

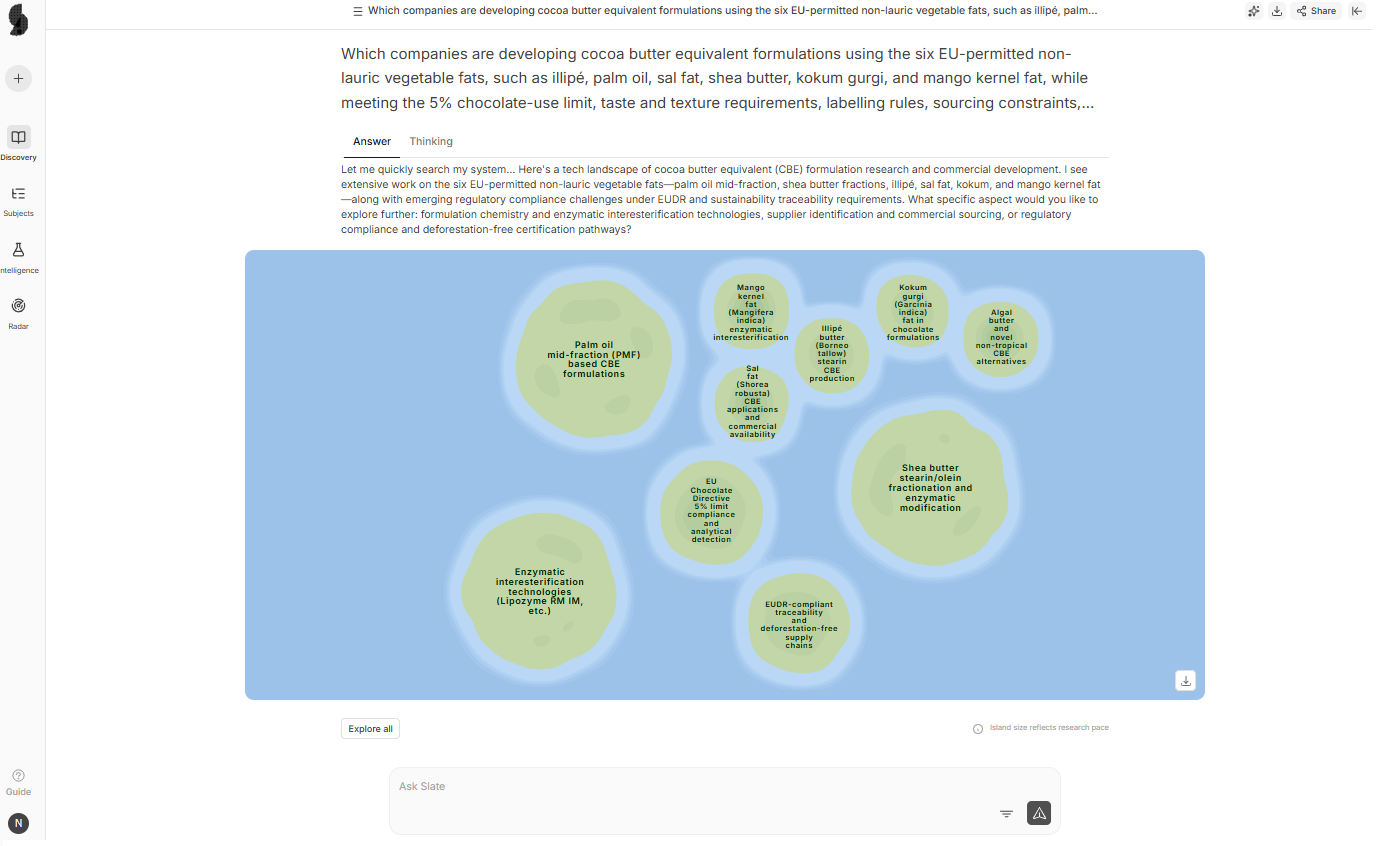

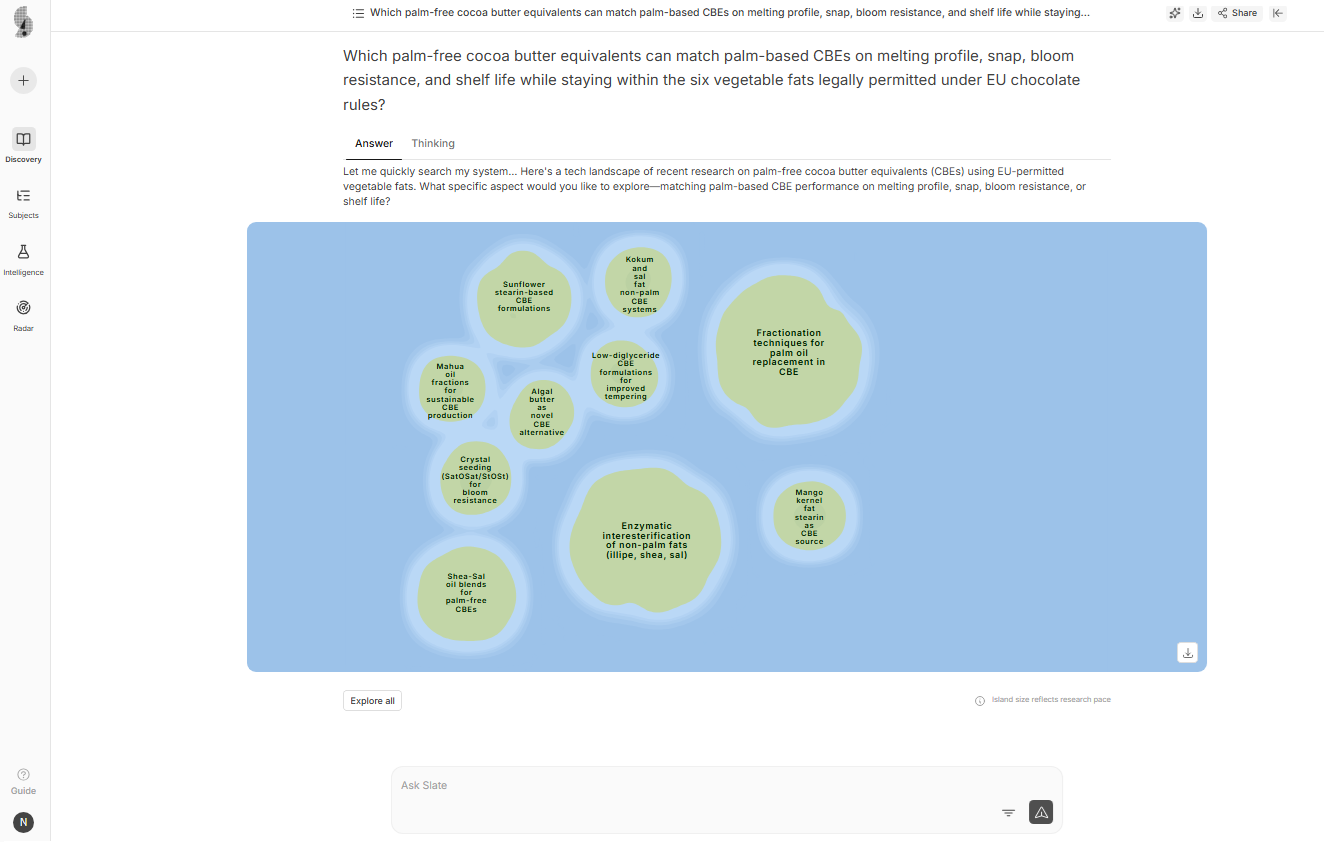

Only Six Vegetable Fats Are Legally Permitted

Not every vegetable fat can be used as a cocoa butter equivalent in chocolate. Under EU rules, only six specific non-lauric vegetable fats are allowed. The six permitted fats are:

- Illipé butter, also known as Borneo tallow or Tengkawang, from Shorea species

- Palm oil, from Elaeis guineensis and Elaeis olifera

- Sal fat, from Shorea robusta

- Shea butter, from Butyrospermum parkii

- Kokum gurgi, from Garcinia indica

- Mango kernel fat, from Mangifera indica

Under EU food law, CBEs can be added to chocolate at up to 5% of the total fat content without affecting the product’s legal designation as “chocolate,” provided they are disclosed on the label.

This legal list matters because palm-free CBE development cannot simply use any alternative fat. Companies need to work within this approved group while still meeting performance, taste, texture, labelling, sourcing, and EUDR compliance requirements.

The Compliance Gap Palm Oil Companies Face

For palm oil companies, the EUDR challenge is not only technical. It is also operational. Proving that palm oil is deforestation-free requires much more than a supplier declaration or a basic sustainability certificate.

Under EUDR, operators need to submit high-precision geolocation coordinates linking products to specific plots of land, alongside evidence of legal, deforestation-free production. Manual spreadsheets cannot scale to meet EUDR’s high data standards, and automated systems are required to validate supplier data and maintain audit-ready records.

Companies can face fines, market bans, and even seizure of goods. EU member state authorities are expected to carry out checks on companies placing regulated products on the EU market.

The EUDR also contains a critical nuance that CBE manufacturers need to understand precisely. In the case of agri-food products, due diligence under EUDR is only required for the commodity directly related to the product as classified under Annex I.

For example, a chocolate bar may contain cocoa, cocoa butter, and palm oil, but as the relevant commodity for chocolate is cocoa, the due diligence obligations are only required for cocoa.

This means that for finished chocolate products, palm oil’s EUDR exposure is narrower than for operators who are placing raw palm oil or its direct derivatives on the EU market as a standalone product. But CBE manufacturers who sell their palm-based fats as intermediate ingredients into the food chain do face direct EUDR obligations for those products, and that compliance cost will flow through to the chocolate manufacturers who buy from them.

Why Palm-Free CBEs Are Gaining Attention

The shift toward palm-free CBE formulations is not a future scenario. It is underway, and it is accelerating.

Major players such as Cargill and Bunge Loders Croklaan are investing in sustainable cocoa butter equivalents derived from shea, palm mid-fractions, and illipe, which help reduce land-use pressures.

Companies like AAK AB in Sweden, one of the world’s leading specialty fats producers have been systematically repositioning their CBE portfolios toward shea and other non-palm sources for several years, anticipating exactly the regulatory shift that is now arriving.

In July 2024, Banj launched Cobrain 206, a shea-based cocoa butter equivalent specifically designed to solve soft chocolate and technical challenges in the ganache market, offering what the company describes as a soufflé-like texture for premium soft chocolate applications.

The shea butter segment is expected to witness the fastest growth rate from 2025 to 2032, driven directly by EUDR-related reformulation demand. The Asia-Pacific CBE alternatives market is projected to grow at the fastest CAGR of 13.4% from 2025 to 2032, driven by rapid urbanization, expanding middle-class populations, and the rising consumption of chocolate and bakery products.

Notably, manufacturers exporting to Europe from Asia face their own EUDR-induced pressure to reformulate, as they need their European market products to be deforestation-compliant.

A Forest 500 Report in 2026 noted that the EUDR “has already steered business expectations, galvanised investment and driven supply chain action by some of the most influential companies in the deforestation economy,” with 313 out of 500 assessed companies having taken some steps to address deforestation.

Taken together, these signals show that palm-free CBEs are no longer a niche reformulation idea. Suppliers are investing, brands are testing, and exporters are preparing. The companies that move early will have more time to secure supply, validate performance, and build products that are ready for both regulation and customer scrutiny.

Why 2026 Is the Critical Window for Palm-Free CBEs

The pre-EUDR period gives ingredient companies and chocolate manufacturers a real first-mover opportunity. But that window is getting smaller.

| Category | Requirement | Date/Deadline | What it Means |

| EUDR enforcement deadline | Large and medium-sized operators must comply with EUDR | 30 December 2026 | Companies placing covered commodities or products on the EU market must meet due diligence, traceability, and deforestation-free requirements. |

| EUDR enforcement deadline | Small and micro enterprises get an extended compliance period | 30 June 2027 | Smaller companies receive additional time before full compliance obligations apply. |

Companies that complete formulation trials, scale up procurement, and qualify palm-free CBEs with customers before the deadline will be in a stronger position.

Once a chocolate brand approves a new fat system, it is not easy to replace it quickly. This gives early suppliers a clear commercial advantage, especially with premium chocolate brands looking for clean-label and deforestation-free ingredient stories.

Supply is another reason to move early. Alternative CBE sources such as shea and sal need stronger sourcing, certification, and traceability systems before they can scale. Supplier readiness will be critical because palm-free CBEs need both technical validation and audit-ready documentation.

Recent EUDR simplification measures may reduce some near-term compliance costs. The European Commission’s May 2026 review says these measures could cut annual compliance costs for companies by about 75% compared with the original EUDR design. Still, the core requirements remain. Companies will need reliable traceability, due diligence, and documentation systems.

So, EUDR may become easier to implement, but it is not going away. For palm-free CBEs, 2026 is a short but valuable window. Companies that use this time to validate formulations, secure certified supply, and build customer trust will be better prepared as regulatory and buyer pressure increases.

What Companies Should Be Doing Right Now

For CBE manufacturers and their customers in the chocolate, cosmetics, and bakery sectors, the strategic actions break down along a clear timeline.

Between now and the end of 2026, the priority is completing the formulation and qualification work.

Palm-free CBE blends using shea, sal, mango kernel, and illipe combinations can match the functional performance of palm-based equivalents for most applications. However, they require trials to verify crystallization behavior, shelf life, and sensory profile in specific product contexts.

Getting this work done before the December deadline means having qualified alternatives ready to activate.

Simultaneously, procurement teams need to be mapping and pre-qualifying supply chains for non-palm feedstocks. Shea supply chains in West Africa are well-developed, but sourcing infrastructure for sal fat, kokum, and mango kernel remains fragmented and requires direct supplier relationships or investment in aggregation systems.

On the palm side, companies that cannot fully exit palm-based CBEs before the deadline need to have their EUDR due diligence systems operational.

The transition in 2026 and 2027 will separate organizations that prepared early from those that underestimated the operational complexity. Waiting until the fourth quarter of 2026 to begin compliance work is not a viable strategy given the data collection and system integration timelines involved.

Finally, companies need to watch the regulatory updates carefully. The European Commission clarified in its May 2026 update that where an agri-food product can be made either from a commodity covered by the EUDR (such as palm oil) or from raw materials that are not covered, only those products made from covered commodities must follow EUDR rules.

This clarification directly benefits palm-free CBE producers by confirming that their products are outside the regulation’s scope, provided they can demonstrate their fat sources are genuinely non-palm.

Conclusion

The EUDR’s arrival is not an isolated policy event. It is part of a broader structural shift in how European markets and their global supply chains will evaluate ingredient sourcing for the foreseeable future.

The UK is developing its own deforestation framework under the Environment Act 2021. Other markets are watching what happens with the EUDR’s implementation as a potential model.

For specialty fats, the convergence of climate-driven supply disruption, regulatory pressure, and consumer demand for transparency has placed palm-free CBE development at an unusually powerful intersection of risk management, commercial opportunity, and genuine environmental purpose.

Shea trees do not require forest clearance. Sal forests in India and Nepal are managed wild stands. Mango kernel fat is a byproduct of the mango processing industry. These are not boutique ingredients, they are scalable, traceable, and technically capable.

The industry has known this for years. The EUDR simply means the question of when to act has finally been answered. The window is open now, but the deadline is December 30, 2026. That is not very far away.

How Slate Helps Identify the Next Palm-Free CBE Opportunity

For companies working on palm-free CBE strategies, the hardest part is not just finding alternative fats. It is knowing which options are technically viable, commercially scalable, and worth acting on before the market moves.

SLATE helps R&D, innovation, and procurement teams track this shift with better intelligence. It can help companies identify emerging palm-free CBE technologies, monitor suppliers working with shea, sal, mango kernel, kokum, and illipé, and compare how different players are responding to EUDR pressure.

It can also support faster decision-making by connecting multiple signals in one place, including patents, product launches, supplier activity, regulatory updates, market movement, and scientific research. For a category like cocoa butter equivalents, this matters because the best opportunities often sit across different data points.

For example, a company exploring shea-based CBEs may need to know which suppliers are expanding capacity, which formulations are being patented, which markets are seeing higher demand, and which regulations could affect future sourcing. Slate can help teams bring these signals together and turn them into practical next steps.

As the EUDR deadline approaches, speed will matter. Companies that can spot reliable alternatives early, validate technical options faster, and track supplier readiness will be better placed to secure supply and avoid rushed reformulation. Slate gives teams the intelligence layer they need to move from reaction to readiness.