For 30 years, salmon was the only PDRN source that mattered clinically. That assumption just broke.

A December 2025 clinical study confirmed that low-molecular-weight peony PDRN improves periorbital skin elasticity in humans. It is the first published topical clinical data for any non-salmon PDRN source in PDRN’s commercial history. The clinical validation gap that protected salmon’s dominance has now started to close.

The timing matters. Less than 12 months before this study appeared, Sephora’s Clean at Sephora programme excluded animal-derived DNA fragments from its certification pathway. That created a structural problem for brands using salmon-derived PDRN. The ingredient still had 30 years of clinical credibility, but it could no longer qualify for one of retail beauty’s most important certification routes.

This is why the plant-based PDRN study matters. It was not driven only by consumer curiosity. It was also a response to certification pressure.

For R&D teams, both barriers have shifted at once. The technical barrier, lack of human clinical validation for plant-based PDRN, is weakening. The commercial barrier, exclusion of animal-derived DNA fragments from certified clean beauty channels, is getting harder to work around.

If your PDRN roadmap depends on certified retail distribution, salmon sourcing now creates a real channel risk. The priority is no longer broad awareness. It is deciding how quickly reformulation needs to begin.

Certification Programmes Built a $26.5B Walled Garden That Salmon PDRN Cannot Enter

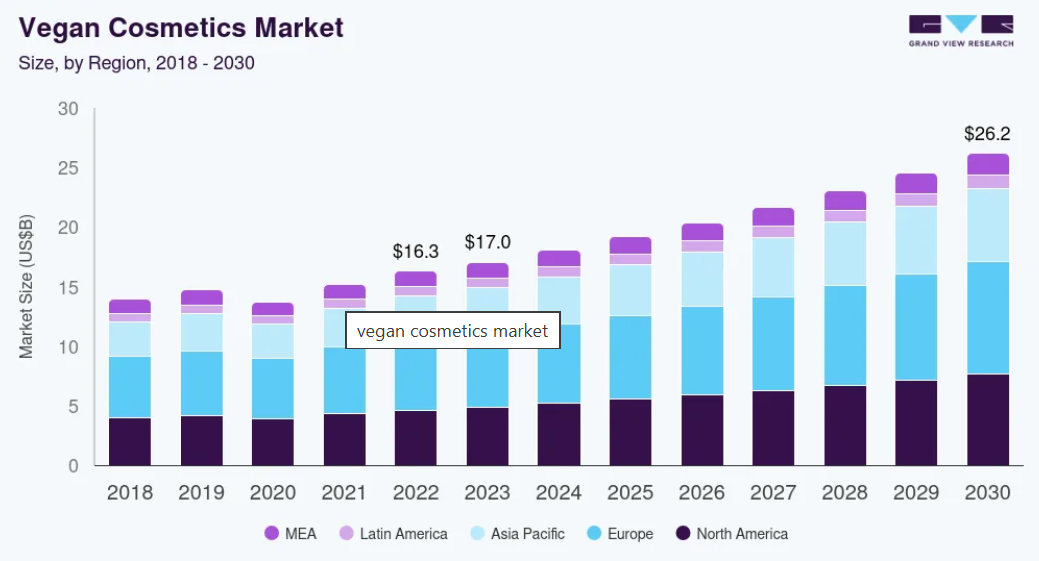

Here’s the thing about vegan cosmetics certification: it isn’t really about consumer preference. It’s infrastructure. The market reached $15.17 billion in 2021 and is on track for $26.2 billion by 2030, but the more important number is the gatekeeping function that programmes like Sephora’s Clean at Sephora, Leaping Bunny, and PETA Beauty Without Bunnies exercise.

These aren’t scoring systems with room for nuance. They’re binary: you’re in or you’re out. And salmon-derived PDRN, however sustainably sourced or clinically validated, is categorically out.

This isn’t a branding challenge. It’s not something you can fix with a “responsibly sourced” label or a sustainability dossier. There is no pathway for animal-derived DNA fragments to earn vegan certification, full stop.

The innovation record tells the story clearly. Of 223 PDRN innovations filed in the past 12 months, 73, roughly a third claim non-marine sources. Three years ago, that figure was negligible. Those 73 filings break down into 51 plant extraction innovations, 16 microbial fermentation methods, and 6 recombinant synthesis approaches, spanning species as varied as barley sprouts, elderberry, arugula, cannabis, seaweed, camellia, rose, and ginseng.

Korean incumbents PharmaResearch and Daewoong built their dominance on salmon-derived IP and three decades of clinical data. That IP carries enormous value in the injectable market. It carries zero value in the certified retail channel. The choice for any brand dependent on retail distribution through clean beauty programmes is binary: reformulate, or exit the channel.

The Clinical Validation Gap Just Closed, and It Happened in China and Korea, Not Europe or the US

The December 2025 peony PDRN study, conducted under Intertek IRB approval, delivered the first human topical efficacy data for any plant-derived PDRN source. It directly refutes the claim that salmon has a clinical monopoly. And it’s not standing alone.

Across the 51 plant extraction innovations filed in this period, specific botanical advantages are now being documented with real technical precision. Rose PDRN (patent WO2026005106A1) claims superiority over salmon DNA in regeneration, wrinkle improvement, and elasticity. Camellia PDRN (CN121873151A) targets MMP inhibition and barrier protein synthesis, with documented anti-photoaging activity. Ginseng PDRN (KR20260045941A) achieves controlled molecular weight precision between 300 and 500 base pairs via a homologous DNase process, enabling application-specific bioactivity tuning that salmon extraction simply can’t replicate.

None of this is speculative. These are published innovations with specific molecular weight control, bioactivity differentiation, and now human clinical data. The clinical moat that protected salmon PDRN for three decades has been crossed.

What’s notable is where this validation is happening. Chinese and Korean small-to-midsize companies are simultaneously validating dozens of plant sources, fragmenting the clinical advantage faster than incumbents can defend it with combination product strategies. Once any ingredient achieves human efficacy data, the remaining differentiators are cost, supply chain reliability, and certification compliance and on all three measures, plant and fermentation alternatives have the structural advantage.

Bloomage Is Running the Hyaluronic Acid Playbook on PDRN, and Korean Manufacturers Have No Answer

Bloomage Biotechnology, with $646 million in annual revenue and STAR Market listing, filed 6 innovations in this period. All target Halomonas and Lactobacillus fermentation pathways. This is the same playbook that made Bloomage the world’s largest hyaluronic acid producer after collapsing the animal-tissue HA supply chain in the 1990s and 2000s.

Bloomage’s choice of Halomonas species is deliberate. This is the same genus they use for exopolysaccharide production, meaning they have deep fermentation optimization data and infrastructure already in place. The company operates a 30,000 square meter pilot facility with 64 production lines, designated a national manufacturing platform in 2025. Fermentation-route PDRN eliminates seasonal variability, geographic supply constraints, and animal-derived regulatory complexity while compressing raw material cost by an estimated 60 to 80 percent.

PharmaResearch and Daewoong, Korea’s dominant injectable PDRN brands, hold zero synthetic production innovations in this dataset. Korean manufacturers’ competitive moat rests entirely on marine-derived PDRN purity and clinical data. Neither of those assets transfers to fermentation route defense, and neither company currently holds fermentation or recombinant production IP.

Additional Chinese players are visible in the fermentation cluster. Hengyu filed 7 innovations, the highest single-company count in the entire dataset, spanning fermentation synthesis, PDRN microspheres, HA-PDRN gel systems, and whitening compositions. Tianjin Saimeng and Guangzhou Youke add further capacity across Bifidobacterium, Lactobacillus paracasei, and Lactobacillus plantarum strains.

If fermentation-route PDRN achieves pharmacopoeia monograph inclusion, as fermentation HA did, it becomes the regulatory reference standard. This would effectively make animal-derived PDRN the non-standard variant, inverting the entire regulatory status hierarchy that Korean manufacturers built over 30 years.

Topical Delivery Validation in 2026 Just Eliminated the Last Scientific Defense Against PDRN Commoditization

PDRN has a size problem. At 50 to 1,500 kilodaltons, its molecules are too large to cross the stratum corneum without assistance. For two decades, this kept topical PDRN in the category of clinical curiosity, confounded by the fact that it couldn’t actually reach the dermis without a needle.

Two 2026 studies changed that. PLGA nanoparticle encapsulation and exosome-based delivery both achieved validated dermis-level penetration in published skin models. The topical penetration problem is solved.

The innovation response was immediate. In the past 12 months: 17 innovations on lipid nanoparticles and liposomes, 9 on microneedle patches, 8 on exosome systems. H&A PharmaChem filed patents on sodium dilauramidoglutamide lysine LNPs, a pharmaceutical-grade RNA delivery vehicle structure for PDRN transdermal delivery. Syoung Cosmetics Manufacturing filed 4 LNP innovations, making them the most prolific filer in this cluster.

But here’s the strategic twist nobody saw coming: solving topical delivery simultaneously commoditised the ingredient itself.

Every high-novelty delivery innovation in this dataset co-loads PDRN with peptides, growth factors, or ceramides. None of them position the delivery architecture as a PDRN-specific vehicle. They position it as an active management platform, a system that can carry PDRN plus whatever else the formulator decides to add. The companies that own the delivery mechanism will control which actives get co-loaded, and on what terms.

This mirrors exactly how HA crosslinking IP shifted value from HA raw material producers to Allergan and Galderma. The ingredient became a commodity. The IP around what you do with the ingredient became the competitive moat.

For undifferentiated PDRN ingredient manufacturers, the math is simple and uncomfortable: once validated LNP, exosome, or microneedle delivery systems are commercially available, your pricing power evaporates. The value migrates to formulators with delivery IP. Retail channels will demand ingredient transparency and efficacy data that only validated delivery systems can provide and that’s a bar that raw material suppliers can’t clear on their own.

Korean Incumbents Are Retreating to the One Segment Certification Cannot Touch, and It May Not Hold

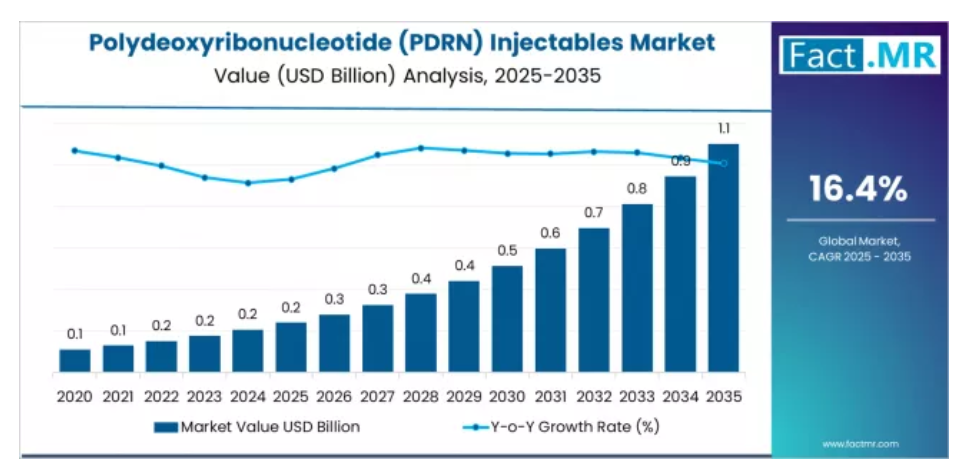

Korean pharmaceutical manufacturers still own the high-value injectable PDRN market, valued at $240 million globally in 2025 and growing to $1.1 billion by 2035 at 16.4 percent CAGR.

This position is based on clinical data and GMP-certified pharmaceutical-grade purification. Salmon-derived PDRN holds a 70 percent share of injectable volume, and pharmaceutical-grade PDRN commands a 5 to 10 times price premium over cosmetic-grade material.

Chinese companies are now developing pharmaceutical-grade salmon PDRN independently. Hengyu, Xingwan Intelligent Manufacturing, Nanjing Letop, and Donghong Yaoxing all filed pharmaceutical-grade extraction innovations in this period. Once validated under NMPA GMP, these producers will seek WHO prequalification to enter regulated Western markets at 40 to 60 percent below Korean price points.

Korean brands will be forced to compete on clinical differentiation, combination products, proprietary delivery formats, and outcome data rather than ingredient purity. PharmaResearch’s August 2025 partnership with Laboratoires VIVACY, a European HA filler manufacturer, signals this pivot. The partnership targets co-development of HA-PDRN combination injectables, building a defensible premium product that combines Korean clinical credibility with European injection expertise. This will likely lock out Chinese HA-PDRN systems from premium European aesthetics despite lower cost.

PharmaResearch’s share price rose approximately 230 percent in the past year, but the company holds zero new R&D filings in this dataset. The company is investing commercially, not in new IP. This is a holding strategy, not a growth strategy. If your competitive position depends on pharmaceutical-grade salmon PDRN purity, Chinese GMP manufacturing will compress your B2B pricing power within 3 years, forcing a pivot to combination products, proprietary delivery, or clinical outcome data as the only remaining differentiation levers.

What This Means for Your Team

Audit your PDRN product roadmap against retail certification programme requirements now, not sustainability messaging or responsibly sourced positioning. If Sephora Clean at Sephora, Leaping Bunny, or PETA certification is required for your target retail channel, salmon-derived PDRN is a categorical exclusion regardless of clinical data, and reformulation lead time is 12 to 24 months once plant or synthetic alternatives achieve clinical validation.

Pressure-test whether your competitive moat is ingredient purity or delivery architecture, because topical delivery validation just shifted value capture entirely to formulators and delivery-IP holders. If you manufacture undifferentiated PDRN ingredients, your pricing power collapses the moment validated LNP, exosome, or microneedle delivery systems become commercially available and co-load competing actives.

Monitor Bloomage’s fermentation PDRN platform for pharmacopoeia monograph inclusion. If synthetic PDRN achieves the same regulatory reference status that fermentation HA did, animal-derived PDRN becomes the non-standard variant, inverting three decades of clinical and regulatory positioning and eliminating the last scientific argument for marine sourcing.

Evaluate whether pharmaceutical-grade injectable PDRN justifies your current R&D spend, given that Chinese GMP-grade salmon extraction is now visible and will compress B2B pricing by 40 to 60 percent once WHO-prequalified, and given that Korean incumbents are already pivoting to combination products as the only defensible margin structure.

Reconsider therapeutic PDRN applications (orthopedic, gastrointestinal, ophthalmology) as the only whitespace with 10 to 50 times cosmetic pricing power. Fewer than 10 innovations address non-aesthetic clinical indications despite validated mechanisms and existing wound-healing clinical data, representing a near-empty competitive field with reimbursement eligibility and hospital procurement access unavailable to cosmetic products.

The Strategic Fork Is Visible

The core strategic tension isn’t whether salmon PDRN will survive vegan certification exclusion in retail cosmetics. It demonstrably won’t that outcome is already structurally determined. The question is whether the pharmaceutical-grade injectable segment can sustain premium pricing once Chinese GMP manufacturing, fermentation cost compression, and topical delivery validation converge simultaneously.

Korean manufacturers have 30 years of clinical data. The question is whether that translates into defensible combination product IP, or whether it simply delays commoditisation by three to five years while competitors build the infrastructure to undercut them on every other dimension.

The certification barrier created the fracture. The fermentation platform is executing it. The delivery architecture shift is erasing the last moat. What remains is a choice: compete on delivery and combination product differentiation now, or defend ingredient purity until the margin structure collapses on its own timeline.

The window to make the first choice is still open. It is not indefinitely open.

Slate: R&D Intelligence That Moves Faster Than the Market

The fracture described in this guide didn’t appear in a market research deck. It appeared in patent filings, clinical trial registrations, and regulatory submissions months or years before it became visible in product launches or pricing pressure. By the time it shows up in a market report, the window to act has usually already narrowed.

That’s the problem Slate was built to solve.

Slate is an AI-powered R&D intelligence platform that tracks exactly the signals that precede strategic shifts: patent filing velocity, clinical trial registrations, regulatory submissions, and supply chain repositioning across pharmaceutical and cosmetic ingredients. It surfaces competitive moves while they’re still moves not after they’ve become market facts.

For teams managing PDRN pipelines specifically, that means knowing when Bloomage’s fermentation platform crosses from experimental to commercial-scale before the price compression hits your margins. It means tracking delivery IP filing velocity LNPs, exosomes, microneedles before those systems become the products your retail buyers demand. It means auditing your ingredient roadmap against live certification programme requirements, not last year’s guidance.

The brands that will hold margin through this transition aren’t the ones with the best ingredients. They’re the ones who saw the shift coming early enough to do something about it. Slate is how R&D teams develop that kind of foresight not as a one-time report, but as an ongoing competitive intelligence capability built into how they work.

If your competitive position depends on understanding where the margin structure is moving, not where it has been, explore what Slate can surface for your category.