Around 12% of U.S. adults have used a GLP-1 drug such as semaglutide, tirzepatide, or a similar medication, and about 6% are using one today. These drugs reduce appetite and slow digestion, which means many users now eat much smaller portions than before.

That shift is creating a new problem for food and beverage companies. People may be eating less, but their bodies still need enough protein, fiber, vitamins, and minerals to stay healthy. In other words, every bite now has to work harder.

This is why fiber fortification is becoming a central part of GLP-1-focused food innovation. For these users, fiber is not just a label claim or a marketing feature. It can help smaller meals feel more satisfying, support the gut microbiome during lower calorie intake, and ease common digestive issues such as constipation linked to GLP-1 use.

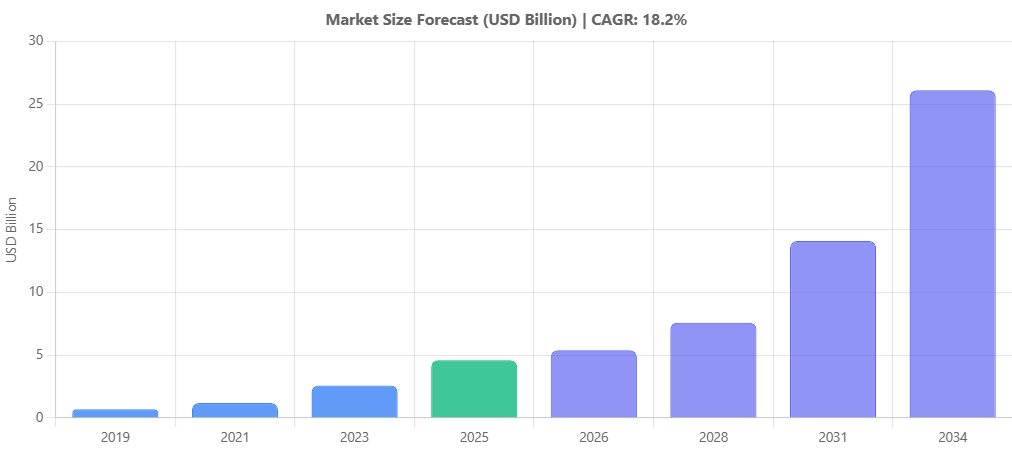

The market is already responding. The GLP-1-influenced food and beverage market reached $4.6 billion in 2025 and is expected to grow at an 18.2% CAGR to $26.1 billion by 2034. This growth is pushing companies to reformulate products, file new patents, and invest in research across dietary fiber science, gut health, and food technology.

This analysis maps where the science is moving, where companies are focusing their innovation, what regulatory limits apply, which technical problems remain unsolved, and where the strongest white spaces are for companies that act before the category becomes crowded.

Why Fiber Fortification Is Becoming Critical in GLP-1 Foods

1. The Portion-Size Paradox

The fundamental formulation challenge GLP-1 drugs create is unprecedented in food industry history. Users must obtain adequate protein, fiber, and micronutrients from eating occasions that are 40–50% smaller in volume than before. Fiber requirements do not shrink proportionally with caloric intake; if anything, the physiological need intensifies:

- Gut motility slows under GLP-1 medications, increasing constipation risk

- Caloric restriction alters the microbiome, increasing dependence on prebiotic inputs

- Satiety extension through fiber becomes the primary mechanism making smaller portions feel complete rather than insufficient

Delivering functional fiber levels of 10 to 20 grams per serving into formats one-third the conventional size is technically demanding in ways that standard fortification approaches do not resolve.

2. Technical Challenges in Matrix Integration

Fiber’s physical chemistry creates problems at every manufacturing stage:

- Bakery: Fiber addition reduces gluten strength by 12.4% and prolongs network development time by 24.4% versus unfortified controls

- Pasta: 20% fiber fortification increases cooking loss by 73% while degrading chewiness, cohesiveness, tensile strength, and elongation

- Extrusion formats (snacks, cereals, bars): moisture rises, expansion ratio drops, air cell size diminishes, and extrudate density increases with die temperature and motor torque becoming unpredictable at industrial scale

3. Sensory and Shelf-Life Compounding Factors

GLP-1 users experience genuine changes in how food tastes and feels. Approximately 75% report heightened sweetness sensitivity, describe conventional products as “sickly sweet,” and develop aversions to rich, fatty aromas and heavy textures. This physiology directly conflicts with fiber’s known sensory liabilities: darkened color, increased hardness, and bitter or earthy off-notes.

Consumer acceptance thresholds exist for every format wheat-rye bread tolerates up to 20% oat fiber fortification before rejection; chicken nuggets cap out around 6% and those thresholds tighten further when sensory physiology has already been altered by the drug.

Research Activity Overview: Volume, Velocity, and Strategic Divergence

1. Strong Upward Publication Trajectory

A bibliometric analysis of 21,434 dietary fiber research articles published between 2010 and 2024 documents a steady upward trend, with acceleration particularly pronounced in the last five years:

- Semaglutide-focused research peaked in 2022 after a sharp rise from 2014

- Gut microbiota research linked to type 2 diabetes and GLP-1 mechanisms hit 1,004 analyzed articles in that same peak year

- Functional foods research for diabetes management reached 1,226 Scopus-indexed articles, with major growth inflections beginning in 2012

2. Academic vs. Industry Research: A Strategically Important Split

Academic institutions dominate publication output. The University of Copenhagen, Spain’s CSIC, and the USDA are leading contributors publishing primarily in Nutrients, Foods, and Food Chemistry. Their work focuses on the mechanistic understanding of fiber-microbiome-GLP-1 interactions.

Industry is concentrating activity in patent filings rather than open publication. Mars Incorporated, Meiji Co., Nestlé, Nutricia NV (Danone), and multiple ingredient suppliers have filed substantial patent portfolios targeting fiber-GLP-1 formulation applications.

Fundamental mechanistic knowledge is being generated in public science while commercial differentiation shifts toward proprietary formulation processes and ingredient IP.

3. Emerging Research Hotspots

Beyond traditional soluble/insoluble fiber classifications, three specific directions are driving the leading edge:

- Engineered probiotics capable of directly modulating GLP-1 secretion

- Structure-defined fiber libraries with glycomically characterized molecular architectures

- Prebiotics as a therapeutic class in their own right, not merely nutritional support

Technologies Shaping the Next Generation of GLP-1 Fiber Foods

1. Enzymatic Fiber Modification: Solving the High-Dose Inclusion Problem

One of the most commercially significant research directions targets the viscosity and off-flavor problem that limits practical fiber inclusion.

Enzymatic modification, particularly depolymerization, converts high-molecular-weight plant polysaccharides into short-chain oligosaccharides that retain prebiotic activity and satiety function while eliminating texture, opacity, and taste liabilities.

One Bio’s proprietary process uses metal-catalyzed oxidative depolymerization to produce “invisible” oat fiber that is tasteless and textureless at 20g+ per-serving inclusion levels. This technology directly addresses the inclusion ceiling that has historically made high-dose fiber fortification commercially unviable across beverage and snack categories.

2. Extrusion-Based Fiber Texturization: Structural Integration Without Degradation

Twin-screw extrusion of wheat bran dietary fiber enhances water-holding capacity, oil-holding capacity, and cholesterol adsorption while improving antioxidant scavenging versus unprocessed bran. Reactive extrusion applied to coffee hull-derived fiber achieves cellulose enrichment without effluent generation, producing ingredients with 45.17% cellulose and 78.20% insoluble dietary fiber content that remain thermally stable to 300°C.

The scalability advantage is significant: extrusion is a continuous manufacturing process that eliminates chemical reagent steps and integrates into existing food infrastructure.

3. Engineered Probiotics: Bypassing Dietary Fiber Entirely

A 2025 study published in Science Advances demonstrated engineered probiotics that release microbial peptides directly into the gut lumen to locally elevate GLP-1 levels, effectively maintaining gut homeostasis in fiber-deficient models.

This approach separates the satiety and metabolic outcomes previously attributed to fiber-microbiome interactions from the need for fiber as the substrate, potentially a lower-inclusion-burden route to equivalent functional outcomes.

4. Structure-Defined Fiber Libraries: Precision Over Empiricism

A 2025 mBio study systematically characterized a highly diverse set of new, highly soluble fibers with varied monosaccharide compositions, glycosidic linkages, and polymer lengths, demonstrating that structure directly predicts both microbial response and metabolic outcomes.

This precision-fiber approach enables ingredient selection based on mechanistic prediction rather than trial-and-error, and creates defensible IP positions around specific molecular architectures rather than generic categories.

5. Microencapsulation: Stability and Controlled Release

High-fiber snack bars stored at 35–45°C show progressive color degradation, moisture instability, and lipid oxidation with calculated shelf lives of only 11 weeks in metalized polyester packaging.

Microencapsulation technologies pairing fiber with hydrocolloid matrices, protein co-processing, or lipid encapsulation systems protect fiber functionality through thermal processing and storage while controlling release kinetics in the GI tract.

The University of British Columbia’s patented microparticle fiber compositions (US2026076398A1) demonstrate the approach’s commercial viability.

6. Upcycled and Fermentation-Derived Fiber: Sustainability as Competitive Advantage

Fermentation-derived prebiotic fibers from brewer’s spent grain, apple pomace, coffee hulls, and other agro-industrial by-products are being characterized for functional performance alongside their sustainability credentials. COMET’s Arrabina™, an upcycled prebiotic fiber derived from arabinoxylan, demonstrates a 23× lower carbon footprint than beta-glucan and 5× lower than conventional chicory root inulin.

Startup and Corporate Innovation Activity

1. Technology Platform Startups

One Bio is the most closely watched ingredient technology company in this space, with a depolymerization process producing short-chain oligosaccharides from oat fiber that are tasteless and textureless at high inclusion doses. Total funding stands at $44.85 million across multiple rounds, with DSM Venturing and Leaps by Bayer in the investor syndicate.

Lembas has developed an AI-driven discovery platform called GLP-1 Edge, which uses machine learning to identify peptides that stimulate endogenous GLP-1 secretion through nutrient-sensing pathways. The platform positions its outputs as clean-label functional food ingredients targeting the body’s native hormone production, rather than drug-adjacent supplements.

2. Consumer Product Startups

Supergut is demonstrating commercial scale for a clinically validated prebiotic fiber brand with 172% year-over-year growth and expansion to more than 5,000 retail doors including Target, Sprouts, GNC, Vitamin Shoppe, and Erewhon. Products are anchored in resistant starch science with published clinical backing, and the patent portfolio covers resistant dextrin/inulin ratio compositions.

3. Corporate Patent Activity

- Mars Incorporated: Patents covering expanded dry products with 15–30% dietary fiber and 20–36% protein for caloric restriction and satietogenic effect directly adjacent to GLP-1 positioning

- Meiji Co.: Patented GLP-1 secretagogue compositions combining fermented milk with specific fiber and oligosaccharide blends

- Nestlé: Filed on fiber-probiotic combinations for microbiome resilience; its Vital Pursuit product line is the most visible CPG launch explicitly designed for GLP-1 users

- Nutricia NV (Danone): Holds patents on fiber compositions for modulating the satiety effects of oral medications, a formulation category with no precedent before GLP-1 mass adoption

Regulatory and Compliance Landscape

United States

The FDA governs fiber-related health claims through:

- 21 CFR 101.76, 101.77, 101.81 covering fiber-containing grain products, soluble fiber, and beta-glucan claims

- FDA’s December 2024 final rule redefining “Healthy” nutrient content claims, updating thresholds for fiber-fortified products

- 21 CFR 104.20 the Fortification Policy, which constrains indiscriminate nutrient addition and misleading claims

No GLP-1-specific food framework currently exists. FDA issued warning letters in December 2024 to supplement companies for unauthorized GLP-1 claims and in March 2026 issued 30 warning letters to telehealth companies for illegal marketing of compounded GLP-1 products.

A September 2025 warning letter to Novo Nordisk for misleading DTC advertising demonstrates that the FDA’s reach extends to even established manufacturers’ promotional practices.

European Union

Under Regulation (EC) No 1924/2006, EFSA has authorized approximately 260 of over 2,300 evaluated claims. Specific fiber thresholds apply:

- “Source of fibre”: 3g per 100g or 1.5g per 100 kcal

- “High fibre”: 6g per 100g or 3g per 100 kcal

In February 2025, EFSA refused to authorize Appethyl® (spinach leaf extract) for weight-reduction claims, a precedent signaling the evidentiary bar for satiety claims remains strict.

The Regulatory Grey Zone: Foods as Drug Companions

The most significant regulatory grey zone is the absence of any framework governing foods marketed as companions to drug therapies. Nestlé’s Vital Pursuit is the canonical example that separates product labeling (nutrient content claims only) from advertising (GLP-1 user references in digital channels).

This bifurcated approach currently works because the FTC governs advertising and the FDA governs labeling. Food Sciences Corp’s US2025177457A1 patent claims a dietary supplement specifically “for individuals undergoing GLP-1 agonist therapy,” illustrating how explicit patent language contrasts with the more careful marketing language brands deploy publicly.

Emerging Scrutiny

FTC enforcement has escalated. December 2025 final order against NextMed imposed $150,000 in consumer refunds for deceptive GLP-1 weight-loss marketing. A September 2025 National Consumers League petition urged an FTC investigation of multiple telehealth platforms, citing 1,200% growth in violative ads from 2022 to 2024.

The “reasonable consumer expectation” standard will evolve as GLP-1 drug penetration deepens when 1 in 8 U.S. adults has used these medications, implicit references to GLP-1 usage contexts in food marketing will be increasingly legible to regulators as drug-adjacent claims.

Key Bottlenecks and Unresolved Challenges in GLP-1 Fiber Fortification

Predictive Models for Multi-Fiber Synergy: Formulators working with fiber combinations currently lack computational models for how those combinations interact in complex matrices. Scale-up costs are substantially higher when formulation parameters cannot be predicted.

Long-Term Stability at High Inclusion Levels: Breakfast cereals with 16% inulin fortification maintain 60-day room temperature stability compressed relative to conventional RTE shelf lives. Whether accelerated aging models accurately predict long-term degradation for novel fiber-fortified formulations remains an open question with direct supply chain implications.

Structure-Function Relationships for GLP-1 Secretion Kinetics: Research has established that structure predicts microbial and metabolic profiles in vitro, but dose-response curves, timing dynamics, and inter-individual variability of GLP-1 secretion in response to defined fiber structures in real-world eating conditions are not mapped with precision sufficient for health claim substantiation.

Scalable Manufacturing for Precision Fibers: The structure-defined fiber libraries that represent the frontier of science are produced through processes of enzymatic fractionation, precise emulsification, and controlled homogenization. It is challenging to scale beyond laboratory and pilot volumes at a commercially viable cost.

Consumer Acceptance Under GLP-1-Altered Physiology: Sensory acceptance thresholds for fiber-fortified products have been established primarily in non-GLP-1 populations. Given documented alterations in sensory physiology associated with GLP-1 drug use, existing thresholds cannot be assumed to translate. Systematic sensory research with GLP-1 user panels is an active gap.

Sustainability and ESG Implications

1. Fiber Sourcing as a Carbon Decision

Life cycle assessment data reveal that fiber ingredient selection carries substantially more carbon leverage than packaging decisions:

- Chickpea hull-derived fiber: 7.62 kg CO₂-equivalents per kg

- Soybean hull fiber: 8.76 kg CO₂eq per functional unit

- COMET’s Arrabina™ (upcycled arabinoxylan): 23× lower carbon footprint than beta-glucan, 5× lower than conventional chicory root inulin

Conventional fiber ingredients and upcycled alternatives are not interchangeable from an ESG reporting standpoint sourcing strategy is an emissions decision.

2. Waste Reduction Through Agro-Industrial By-Product Valorization

Apple pomace functions effectively as a fiber fortificant in high-moisture meat analogs at up to 20% inclusion, simultaneously addressing waste management costs and delivering antioxidant capacity. Coffee hull-derived fiber, processed through reactive extrusion, achieves fiber modification in a one-step process with zero effluent generation.

Sugar beet biorefinery integration demonstrates the circular economy potential: a patented method utilizing the entire beet biomass reduces energy consumption and carbon emissions by 40% per unit while yielding 219g of functional product from 1kg of raw beets versus 120g of refined sugar from conventional processing.

3. Circular Economy Relevance

The integration of dietary fiber extraction into biorefinery concepts is gaining commercial momentum.

Sugar beet processing demonstrates the closed-loop potential: a patented method utilizing the entire beet biomass produces an unrefined sweetener containing 12.9% fiber and 3.45% protein while reducing energy consumption and carbon emissions by 40% per unit versus conventional processing, yielding 219g of functional product from 1kg of raw beets compared to 120g of refined sugar.

New plant breeding technologies applied to chicory root for inulin production retain over 80% of generated value-added within the EU economic zone while improving greenhouse gas and energy metrics simultaneously.

4. Resource Efficiency Metrics

Comparative extraction methodology assessment demonstrates significant efficiency differentials. Water extraction of corn cob fiber yields 98.12% total dietary fiber, outperforming acid and alkali alternatives in oil-holding capacity, swelling capacity, and cholesterol adsorption while avoiding chemical reagent consumption entirely.

Freeze-drying of carambola peel fiber preserves superior physicochemical, nutritional, and hydration properties versus oven-drying while minimizing energy consumption and CO₂ emissions establishing a benchmark for green extraction approaches. These data points establish that manufacturing process selection is itself a resource efficiency decision, not merely a cost optimization.

Strategic White Spaces for Food Companies

1. Clinical Nutrition and Healthcare System Partnerships

GLP-1 drug prescribers endocrinologists, bariatricians, primary care physicians, and hospital nutrition teams have no established dietary protocol for fiber intake management during GLP-1 therapy.

The opportunity for food companies is to enter formal partnerships with healthcare systems for perioperative GLP-1 patient nutrition management, creating clinically sanctioned product categories with physician recommendation channels that bypass consumer marketing regulatory constraints. Medical food regulations (21 CFR 101.9(j)(8)) provide a narrow but potentially valuable pathway.

2. Beverages: The Highest-Upside Format Gap

High-fiber beverages are technically the most constrained and commercially the most attractive white space in this landscape. Conventional soluble fibers create viscosity and opacity at functional doses incompatible with most beverage formats. The commercialization of “invisible” fiber technology directly unlocks this category.

A GLP-1-user-appropriate high-fiber beverage delivering 10–15g per serving with no sensory compromise does not currently exist at commercial scale. The ingredient technology is approaching readiness; the product application is open.

3. Pet Food and Veterinary Nutrition

GLP-1 receptor agonists are entering veterinary medicine semaglutide analogs for dogs are in development trials. The satiety mechanism, microbiome dependence, and fiber formulation logic in GLP-1-using companion animals are directly analogous to the human application.

Pet food is a less regulated, higher-margin category where functional fiber inclusion is technically easier in wet and semi-moist formats. Companies developing formulation expertise in the human GLP-1 food space will be structurally positioned to transfer those capabilities into pet nutrition.

4. Precision Fermentation-Derived Fiber Structures

The structure-defined fiber library approach creates an opportunity for precision fermentation companies to produce fibers with specific prebiotic selectivity profiles optimized for GLP-1 secretion. Unlike agricultural extraction, fermentation enables molecular precision and batch-to-batch consistency.

An ingredient IP position for a structure-defined prebiotic fiber with demonstrated GLP-1 secretagogue activity in human trials would be commercially valuable across multiple CPG relationships.

What Companies Should Monitor

High-dose “invisible” fiber commercialization is the most important near-term signal. One Bio’s supply agreement announcements with major CPG or beverage manufacturers will indicate whether the depolymerized fiber approach is scaling to actual product deployment. Monitor presence at IFT, Fi Europe, and SupplySide West for commercial partnership signals.

AI-driven bioactive discovery is moving faster than traditional development cycles allow. The critical milestones: peer-reviewed validation publications (not company-funded studies alone) and IND or novel ingredient filing activity. A single well-powered human trial demonstrating endogenous GLP-1 elevation from an AI-identified food-derived peptide would reshape the ingredient landscape.

Regulatory trajectory in the grey zone will be clarified within 12–24 months. Track FTC guidance documents on health and wellness marketing claims adjacent to pharmaceutical therapies and whether the FDA initiates formal regulatory proceedings on companion food positioning. As drug penetration deepens, regulatory action against implicit drug-association marketing becomes increasingly probable.

Investment prioritization should favor ingredient technology platforms over finished brands in the near term. The $82.55 billion projected anti-obesity drug market by 2032 creates B2B ingredient demand scaling across multiple CPG customers, structurally superior to single-product consumer brand bets in an active regulatory environment. Target companies with:

- Proprietary fiber modification processes enabling high-dose inclusion without viscosity or sensory degradation

- Demonstrated structure-function relationships linking specific fiber structures to metabolic outcomes

- Existing or in-development CPG partnerships validating commercial readiness beyond the laboratory

Caution: Investment theses dependent on explicit “GLP-1 booster” supplement positioning face the highest near-term regulatory risk and should be approached with material skepticism.

Final Takeaway

GLP-1 drugs are changing how people eat. Smaller portions, reduced appetite, and digestive changes are creating a new food innovation challenge.

Fiber fortification sits at the center of this shift. It can help make smaller meals more satisfying, support gut health, improve digestive comfort, and increase nutrient density.

But success will not come from simply adding more fiber. Companies need better ingredient technologies, stronger clinical evidence, careful claims, and product formats designed around the real eating experience of GLP-1 users.

How Slate Helps Food Innovators Act Faster in the GLP-1 Market

For R&D teams, the challenge is not a lack of information. It is the speed at which the GLP-1 nutrition space is changing.

New papers are being published. Startups are launching fiber technologies. Ingredient suppliers are filing patents. Regulators are watching claims more closely. CPG brands are testing new product formats. By the time these signals appear in market reports, the best opportunities may already be crowded.

Slate helps R&D teams spot these shifts earlier.

It brings together signals from research papers, patents, product launches, startups, clinical studies, supplier activity, and regulatory updates. Instead of tracking each source separately, teams can see where science, technology, and market activity are moving together.

For a food or nutrition company, this means faster and sharper decisions. Slate can help teams identify which fiber technologies are gaining traction, which startups are worth watching, which claims may create risk, and which product formats still have open space.

It can also help researchers move beyond trend spotting. For example, if high-dose invisible fiber is emerging as a beverage opportunity, Slate can help map the science behind it, the companies developing it, the patents surrounding it, and the product categories where it could be applied.

Slate gives R&D teams that early view. It helps them find the right technologies sooner, evaluate risks faster, and act on white spaces before competitors do.