PDRN has become one of the most watched ingredients in regenerative skincare and aesthetic medicine. For years, the competition was straightforward: who had the purest source, the strongest clinical data, the most reliable salmon milt supply chain. That race is still running. But a second, more consequential race has quietly opened alongside it.

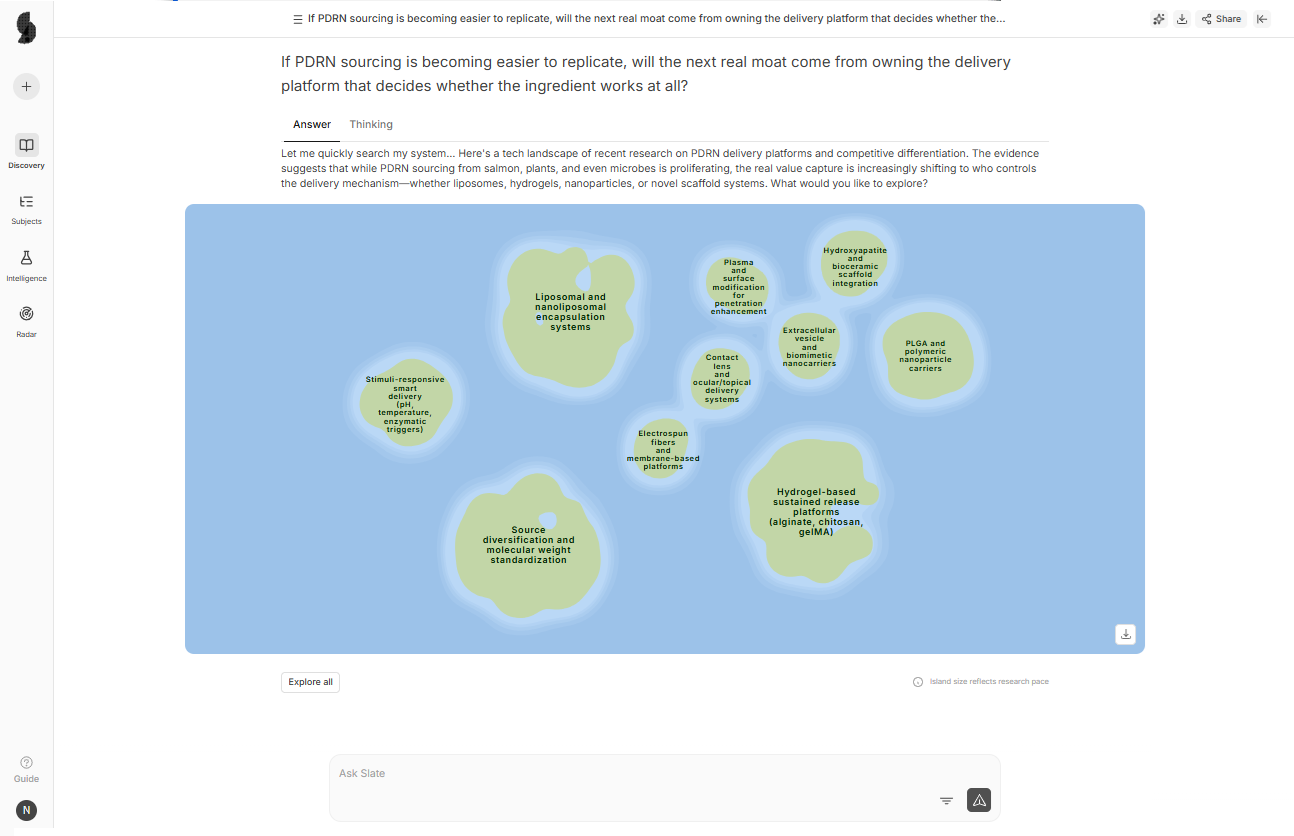

The last 12 months of innovation filings tell the story clearly. Seventeen lipid nanoparticle systems. Nine microneedle platforms. Eight exosome delivery architectures. Together, those delivery-focused filings are approaching the 51 botanical sourcing innovations and comfortably ahead of the 19 focused on extraction purity.

The industry isn’t just growing; it’s reorganizing around a different question entirely. Not what PDRN is, but how to actually get it into the skin.

Two 2026 academic studies gave that shift its scientific foundation. PLGA nanoparticles and exosome encapsulation both demonstrated dermis-level PDRN penetration addressing the core objection that has followed topical PDRN for two decades. At 50 to 1,500 kDa, PDRN molecules are too large to cross the stratum corneum passively. That physical constraint kept the ingredient locked in clinic-only injectables while topical formats remained scientifically questionable. That constraint now has credible solutions.

For R&D and innovation teams, the filing velocity is the real signal. Companies aren’t racing to patent better PDRN. They’re racing to own the platform that delivers it. The next defensible position in this market may not come from the ingredient at all.

This analysis draws on 223 innovations filed over the last 12 months, clustered and mapped using Slate’s AI intelligence platform. Let’s get into details.

Why Topical PDRN Delivery Is Becoming the Next Innovation Race

PDRN injectables have had a strong commercial advantage because they solve the penetration problem by default. Since the molecule is delivered directly into the tissue, injectables can support stronger efficacy claims, remain preferred in clinical settings, and command premium pricing.

Topical PDRN products have had a tougher path.

Without a strong delivery mechanism, much of the active material may remain closer to the skin surface instead of reaching the dermis, where PDRN’s regenerative effects are more relevant. That limits both performance and the strength of product claims.

This is why delivery innovation is now accelerating.

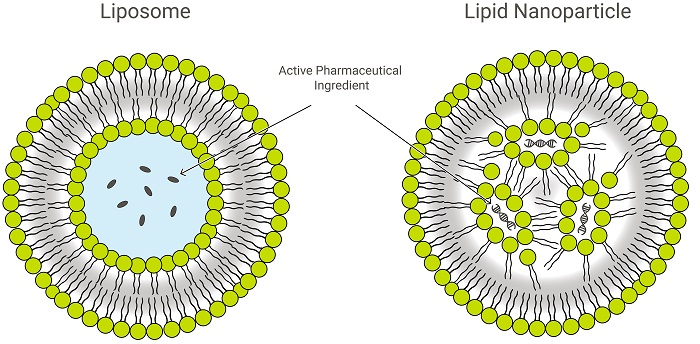

Lipid nanoparticles, liposomes, microneedles, exosomes, and biopolymer carriers are all being explored as ways to move PDRN past the outer skin barrier. Each system has a different technical logic, but they are solving the same commercial problem: how to make topical PDRN credible.

The market opportunity is large. PDRN injectables were estimated at about $240M in 2025 and are projected to reach $1.1B by 2035. But validated topical delivery could open access to the much larger cosmeceutical retail market, estimated at around $80B globally.

That changes the business model.

Injectables may generate $150 to $800 per session in clinics. Topical PDRN products may sit closer to $50 to $150 per product. But topicals can reach a much wider consumer base through retail, e-commerce, and repeat-use routines.

So the value is not only in making PDRN work better. It is in making PDRN scalable.

Delivery Systems Are Being Built as Multi-Active Platforms, Not PDRN-Specific Vehicles

Recent PDRN delivery innovations are not being built around PDRN alone.

Nearly all of them co-claim PDRN with active peptides, growth factors, exosomes, or other supporting actives. That is an important signal. These systems are not just delivery vehicles for one ingredient. They are being designed as multi-active platforms.

This gives delivery IP a much larger role in the value chain.

A company that controls the delivery mechanism can influence which actives are loaded with PDRN, what concentration reaches the dermis, and how those actives are released. That makes the delivery architecture more valuable than any single ingredient. A similar shift happened in hyaluronic acid, where crosslinking IP owned by companies such as Allergan and Galderma became more valuable than HA production IP itself.

The same pattern is now starting to appear in PDRN.

H&A PharmaChem’s lipid nanoparticle systems co-load PDRN with peptides. Exosome systems from Stemon and Bueno Bio carry PDRN with stem cell-derived growth factors. Enzyme-responsive liposomes release PDRN alongside ECM components. These are not simple formulation tweaks. They are platform plays.

The filing data supports this shift. In the last 12 months, the delivery cluster included 17 LNP and liposome innovations, 9 microneedle systems, 8 exosome platforms, and 5 chitosan or biopolymer carriers. That adds up to 39 delivery-focused innovations, compared with 19 innovations focused on extraction purity.

So the competitive battleground is moving upstream. It is no longer only about ingredient quality. It is about delivery architecture.

This changes the position of ingredient suppliers.

If a company sources PDRN as a raw material and places it into a standard emulsion or gel base, it has little control over the delivery architecture. A competitor that licenses a validated LNP or exosome platform and co-loads PDRN with three other actives in a penetration-validated system can create a product that is much harder to match.

That is where platform consolidation becomes important.

If delivery IP holders become the gatekeepers, they can set formulation terms for ingredient suppliers. They can decide who gets access, which actives can be combined, and how the product is positioned. Ingredient suppliers may still own strong process IP, especially Korean marine PDRN extractors and Chinese fermentation producers. But if delivery becomes the bottleneck, their role could shift.

They may move from being premium ingredient owners to raw material suppliers inside a delivery-IP-controlled market.

In that scenario, pricing power and formulation flexibility migrate away from PDRN producers and toward companies that own validated LNP, exosome, and microneedle platforms.

Three Delivery Architectures Are Emerging as Platform Standards and They Are Not Interchangeable

Not all delivery architectures are interchangeable, and the choice isn’t a formulation decision;it’s a regulatory and supply chain commitment for the next three to five years.

Lipid nanoparticles and liposomes are leading in volume (17 innovations) for good reason. They classify as cosmetics in most markets, scale well in manufacturing, and co-load broadly with peptides, ceramides, and antioxidants. H&A PharmaChem’s sodium dilauramidoglutamide lysine LNPs are structurally similar to pharmaceutical-grade RNA delivery vehicles, not a coincidence. The tradeoff: less differentiation in clinical storytelling compared to the other two.

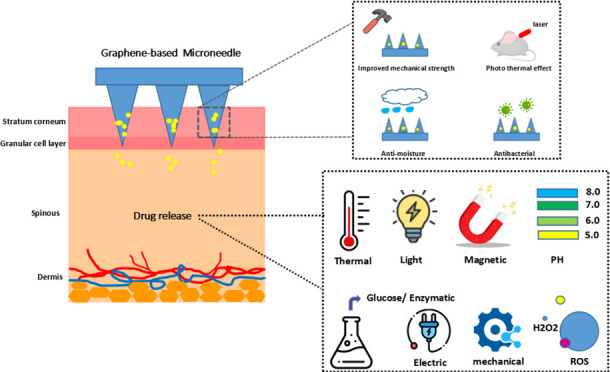

Microneedles are a different proposition. Daewoong Therapeutics’ work claims PDRN concentrations at 6 wt% or higher in dissolving formats well above typical injectable concentrations. Juvic and Catholic University of Korea are developing graphene-reinforced microneedle variants that may facilitate PDRN uptake via electroporation-like mechanisms. Physical delivery proof is compelling, but these systems likely trigger device classification under FDA and EU MDR pathways. The regulatory burden is real. So is the clinical story.

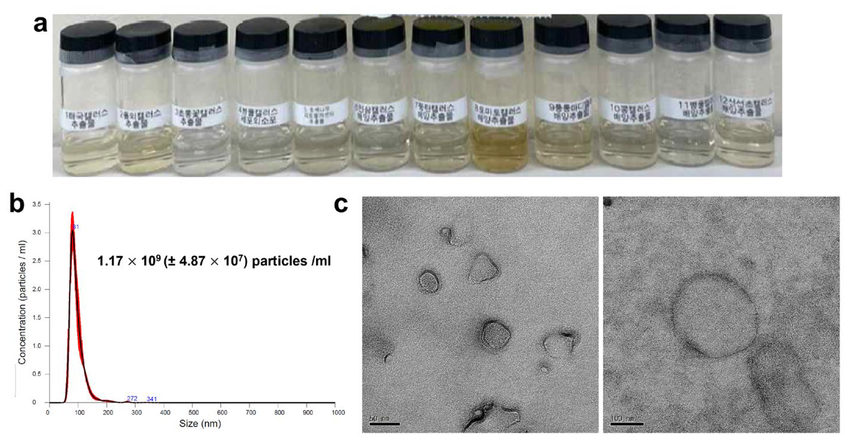

Exosome systems carry the highest novelty ceiling and the most manufacturing complexity. Stemon’s approach extracts both PDRN and PDRN-enriched exosomes from salmon testis in a single process the exosomes carry PDRN in its natural biological context, which is a meaningfully different claim. Umbilical cord MSC-derived nanovesicles add stem cell-derived growth factor co-delivery. These systems face potential biologic classification in major markets and scale poorly due to sourcing constraints. But the mechanistic narrative is unlike anything else in the market.

The Ingredient Supply Chain Is Fracturing and Delivery IP May Be the Only Defensible Moat Left

PDRN’s supply chain is starting to fragment.

For years, salmon-derived PDRN held the strongest position because it had clinical credibility, premium pricing, and established extraction know-how. But that advantage is now being challenged from three directions: plant extraction, microbial fermentation, and recombinant synthesis.

The innovation data shows how fast this shift is happening.

Botanical PDRN extraction now accounts for 51 innovations across sources such as barley, peanut, elderberry, cannabis, ginseng, camellia, and rose. Microbial fermentation adds another 16 innovations, led by Bloomage through Halomonas (CN121203909A), Lactobacillus rhamnosus (WO2025176205A1), and E. coli CGMCC No. 36169 (CN121896143A) strains. Recombinant synthesis adds 6 more innovations.

A December 2025 clinical trial also validated peony-derived PDRN for improving periorbital skin elasticity in humans. That is important because it provides the first published topical clinical data for any plant-derived PDRN.

This creates a real challenge for salmon-derived PDRN.

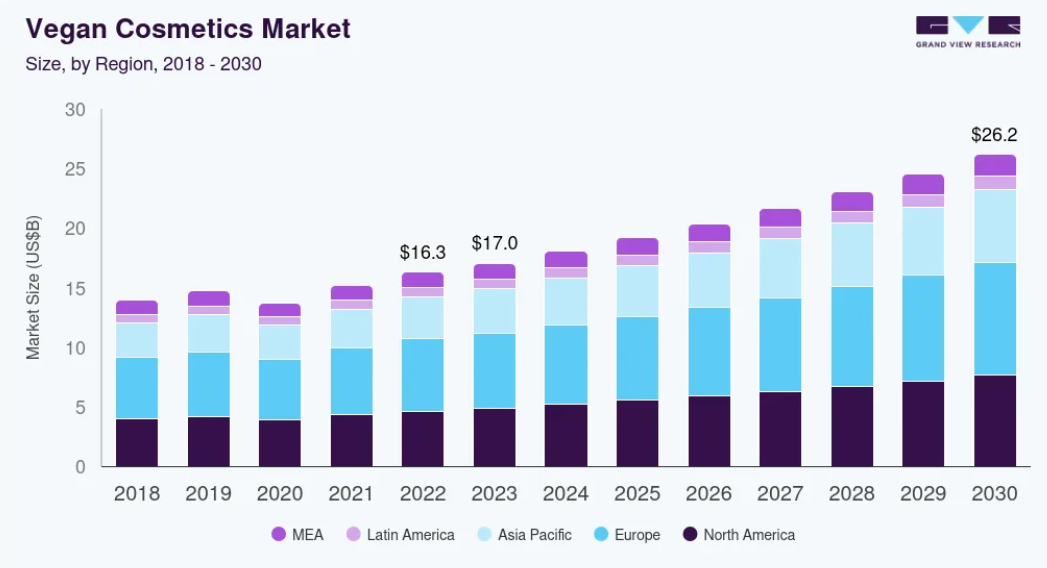

The global vegan cosmetics market size was estimated at USD 15.17 billion in 2021 and is projected to reach USD 26.16 billion by 2030, growing at a CAGR of 6.3% from 2022 to 2030.

Salmon-derived PDRN cannot easily fit into vegan and cruelty-free certification programs such as Clean at Sephora, Leaping Bunny, and PETA. If two or three plant-derived PDRN sources achieve clinical validation and clean-beauty certification in 2026 or 2027, Korean marine PDRN manufacturers could lose access to one of the fastest-growing retail channels.

That would put pressure on both ingredient purity claims and sourcing-based differentiation.

Fermentation could create even stronger disruption.

Bloomage Biotechnology filed 6 fermentation-related PDRN innovations in this period. The strategy closely resembles the company’s earlier move in hyaluronic acid, where microbial fermentation helped replace animal-derived HA and pushed the market toward lower cost, higher consistency, and larger-scale production.

Bloomage became the world’s largest HA producer, with $646M in annual revenue. It also operates a 30,000 square meter pilot fermentation facility with 64 production lines. If the company can scale PDRN fermentation in the same way, raw material costs could fall by 60 to 80%, and market power could shift from Korean marine extractors to Chinese fermentation producers within five years.

That is why delivery IP is becoming so important.

If a PDRN product’s differentiation depends only on pharmaceutical-grade salmon milt extraction, GMP-certified purity, or sourcing credibility, that moat may weaken as alternative sources mature. Multiple challengers are already working to replicate or undercut that advantage through plant-derived, fermentation-based, and recombinant PDRN.

Once two or three alternative sources gain clinical validation, ingredient scarcity becomes harder to defend.

At that point, the stronger competitive advantage may sit in delivery architecture. The companies that own validated LNP, exosome, microneedle, or other delivery platforms will have more control over product performance, formulation flexibility, and long-term differentiation than companies competing only on the source of PDRN.

Delivery Platform Ownership Equals Co-Loading Control and That Is the Real Business Model

The companies that own validated PDRN delivery IP may control far more than product performance. They may control how ingredient suppliers access the dermis.

That is the real business model emerging here.

A validated delivery platform can set the terms for which actives are loaded with PDRN, how they are combined, what concentrations reach the dermis, and how the final formulation is commercialized. This creates room for per-active licensing fees, co-formulation royalties, and exclusivity agreements.

In that model, the platform owner does not extract value only from PDRN. It can extract value from every ingredient supplier that wants validated transdermal access.

That is why a delivery platform could become 10 to 50 times more valuable than a single-ingredient product line.

PharmaResearch’s August 2025 partnership with Laboratoires VIVACY shows where this is heading. The collaboration brings a major European HA filler company directly into the PDRN space through HA-PDRN combination injectables. At the same time, 11 innovations around covalent PDRN-oxidized HA crosslinked gel systems show that the market is moving toward more advanced combination platforms.

These systems may also require distinct regulatory approval under EU MDR and US 510(k) or PMA pathways. That makes the delivery architecture more than a formulation choice. It becomes part of the product’s regulatory and commercial identity.

Exosome platforms show the same pattern. They can co-load PDRN with stem cell-derived growth factors and ECM components in a single delivery architecture. Companies such as Stemon and Bueno Bio are not just creating PDRN products. They are building systems that decide which actives can travel with PDRN and under what commercial terms.

Merck GmbH’s filings add another layer to this shift.

The company filed two innovations around viscosity-reducing excipients for high-concentration nucleic acid injectables. These are pharmaceutical-grade formulation technologies, not cosmetic formulations. If PDRN moves deeper into therapeutic injectables, this kind of excipient IP could become a formulation toll gate for pharmaceutical-grade PDRN products.

Merck does not need to manufacture PDRN, run clinical trials, or build a consumer brand to capture value. It only needs strong formulation IP that other product developers may need to license.

This creates a clear warning for companies developing standalone PDRN formulations.

If you do not own or license the delivery platform, you may end up operating inside someone else’s platform. That means paying licensing fees for dermis access, accepting co-formulation restrictions, and competing with other ingredient suppliers trying to use the same delivery architecture.

In that scenario, the platform owner captures the margin while ingredient suppliers compete for access.

Western Pharmaceutical IP Is Already Positioning for a Platform Tax

Western pharmaceutical companies are not leading the visible PDRN ingredient race. Korean and Chinese companies still dominate most activity around extraction, fermentation, cosmetic formulations, and delivery patents.

But Western players may be positioning themselves at a different layer of the value chain: formulation infrastructure.

Merck GmbH’s two innovations on viscosity-reducing excipients are a strong signal. These filings target high-concentration nucleic acid liquid formulations and include excipients such as arginine, phenylalanine, ornithine, and meglumine.

These are not cosmetic formulations. They are pharmaceutical-grade injectable formulation technologies for nucleic acid therapeutics.

That matters because therapeutic PDRN products will face very different requirements from cosmetic injectables. If PDRN moves into mainstream pharmaceutical applications such as injectable cartilage repair, gastrointestinal treatments, or wound biologics, the formulation will need to meet stricter standards for stability, viscosity, and injectability.

Those products may also move through FDA or EMA approval pathways, especially in orthopedic, gastrointestinal, and therapeutic wound-healing indications. In that setting, formulation performance becomes more than a technical detail. It can become a regulatory requirement.

This is where Merck’s excipient IP could become important.

If its viscosity-modulating system becomes necessary to achieve the concentration stability and injectability required for approval, Merck could sit in a powerful licensing position. The company would not need to manufacture PDRN, run clinical trials, or build a PDRN brand. It could still extract value by owning the formulation layer that therapeutic-grade PDRN products may need.

That is the platform tax strategy.

Asian companies may continue to lead the ingredient and cosmetic formulation race. But Western pharmaceutical companies appear to be bypassing the ingredient layer and staking IP on infrastructure that future therapeutic PDRN products may not be able to avoid.

For companies developing PDRN injectables beyond aesthetics, this is an early warning.

If your roadmap targets cartilage repair, wound biologics, gastrointestinal applications, or other therapeutic indications, you may need to assess whether your formulation can avoid Merck’s viscosity-modulating excipient IP or whether licensing becomes necessary later.

The platform tax is being positioned before therapeutic PDRN reaches commercial scale.

What This Means for Your Team

Audit your PDRN roadmap for delivery IP ownership or licensing. If your pipeline treats PDRN as a raw material added to standard serums, emulsions, or gel bases, it may depend on a weaker penetration mechanism. The 2026 studies on PLGA nanoparticles and exosome encapsulation show that validated delivery systems can improve topical PDRN performance. Teams should prioritize delivery platform partnerships, licensing agreements, or in-house LNP development before competitors secure exclusive positions.

Review sourcing contracts with a three to five year commoditization lens. The landscape now includes 51 botanical extraction innovations, 16 microbial fermentation innovations with Bloomage leading the charge using the same playbook that disrupted animal-derived HA, and 6 recombinant synthesis innovations all converging on lower-cost non-marine PDRN. The December 2025 peony clinical trial delivered the first human efficacy data for plant-derived PDRN. If your contracts are built on salmon-derived scarcity pricing, they are worth revisiting now.

Pressure-test where your PDRN moat really sits. If your differentiation depends mainly on pharmaceutical-grade salmon milt extraction, GMP-certified purity, or clinical data for PDRN alone, that advantage may weaken. Challengers are already working on fermentation and plant-derived sources that could replicate or undercut that purity at 60 to 80% lower cost. IP investment should shift toward delivery platforms, where the moat is more structural and harder to replace through alternative sourcing.

Flag therapeutic PDRN indications as high-value whitespace. The innovation record shows fewer than 10 filings across orthopedic, gastrointestinal, and ophthalmologic therapeutic applications, even though PDRN’s adenosine A2A mechanism supports anti-inflammatory and regenerative activity. These indications may offer 10 to 50 times the pricing premium of cosmetic uses. For teams with clinical development capability, cartilage repair, diabetic neuropathy, and post-surgical adhesion prevention could offer first-mover opportunities before platform consolidation limits access.

Monitor Merck’s excipient IP if your roadmap includes therapeutic-grade PDRN injectables. Merck GmbH’s viscosity-reducing excipient innovations for high-concentration nucleic acid formulations could become important formulation enablers for PDRN products targeting FDA or EMA approval. Teams should assess whether their formulation can route around this IP or whether early licensing may be strategically safer.

The Consolidation Question No One Can Answer Yet

The unresolved strategic question is not whether delivery systems will dominate PDRN product value. The 2026 peer-reviewed penetration data and 39 delivery innovations in 12 months have settled that. The question is whether the industry will consolidate around two to three delivery platform standards with oligopolistic licensing terms, or fragment into dozens of incompatible delivery architectures that prevent co-loading standardization. Fragmentation would leave formulators negotiating bespoke deals with every platform holder, ingredient supplier, and excipient IP owner simultaneously. That market structure would make therapeutic-grade PDRN injectables commercially unviable despite clinical validation.

You must choose a delivery platform positioning within 12 to 24 months before the consolidation window closes. Own the platform, license it, or build it in-house. The correct choice depends on a market structure question no single company controls and that will only become clear retroactively. But delivery IP ownership in any validated architecture is structurally more defensible than ingredient sourcing as the PDRN supply chain commoditizes.

Need to map competitive delivery IP positions or identify undefended platform opportunities before the window closes? SLATE – AI R&D intelligence platform surfaces the technical architecture clusters, filing velocity signals, and whitespace gaps that define where delivery platform value is concentrating. Run the same analysis for your development roadmap.