Precision fermentation is moving from early technical promise to commercial scale-up. GFI notes that fermentation-enabled protein production has expanded from a niche area into a global food solution producing bioidentical animal proteins and functional ingredients. In 2025, more than 163 specialized companies were active in the sector, while companies in the fermentation ecosystem raised $632 million in 2024.

The challenge now is cost and scalability. Published techno-economic models for precision fermentation-derived proteins show a wide cost range, from below $20/kg to $14,000/kg, reflecting how strongly production economics depend on strain performance, feedstock choice, process design, and recovery methods. GFI also identifies feedstocks, raw materials, facility capital costs, process metrics, titer, productivity, and downstream recovery as key cost levers.

This article examines the challenges slowing precision fermentation in alternative protein, the new opportunities emerging across feedstocks, processing, B2B ingredients, and hybrid products, and what R&D teams should do next to move from lab success to scalable food ingredients.

Precision Fermentation is Entering a Harder Commercial Phase

Precision fermentation uses engineered microorganisms to produce specific proteins or functional molecules without animal agriculture. In alternative protein, this includes whey, casein, ovalbumin, collagen, myoglobin, heme proteins, enzymes, fats, and other functional ingredients.

The technology has already shown commercial promise. Dairy proteins are the most mature application area, followed by egg proteins and meat-related functional ingredients. Companies are also moving toward B2B ingredient models, where fermentation-derived proteins are sold into existing food systems rather than launched only as consumer-facing products.

But the next phase is more demanding. R&D teams must improve strain productivity, reduce downstream costs, secure feedstock flexibility, prove food functionality, and prepare safety data for multiple regulatory markets. The field is shifting from “can we make it?” to “can we make it repeatedly, affordably, and at scale?”

Now let’s get into challenges in precision fermentation for alternative protein.

Top Challenges in Precision Fermentation for Alternative Protein

Challenge 1: Strain productivity is still not high enough

Strain engineering remains the first barrier to commercial success. The production organism must deliver high titer, high yield, and stable productivity across repeated fermentation runs. It must also produce proteins with the right folding, structure, and functionality for food use.

The technology landscape has consolidated around Komagataella phaffii, formerly Pichia pastoris, and Saccharomyces cerevisiae as leading food-grade platforms. These organisms have strong genetic toolkits and regulatory familiarity. Still, complex proteins remain difficult. Egg proteins show the gap clearly: ovalbumin has reached 3.7 g/L in E. coli EcN, while ovomucoid has reached 3.2 g/L in K. phaffii, far below the levels needed for broad cost competitiveness.

New strain engineering approaches are addressing this gap. These include genome-streamlined chassis, protease-deficient hosts, multi-copy gene integration, molecular chaperone engineering, secretion optimization, and AI-guided strain design. Machine learning is becoming especially relevant because it can shorten strain development cycles and identify edits that improve secretion or productivity.

| Strategic Implication: |

R&D teams should map every target molecule against the right host, expression system, secretion route, and downstream burden. A protein that looks attractive on paper may fail commercially if the host cannot produce it at scale or if recovery becomes too expensive. |

Challenge 2: Scale-up changes the biology and the economics

A process that works in a lab does not always survive scale-up. Larger bioreactors introduce oxygen transfer limits, pH gradients, heat transfer issues, foaming, shear stress, contamination risk, and uneven nutrient distribution. These factors can lower productivity and affect product quality.

High cell density fed-batch cultivation remains the dominant industrial approach, but it requires tight process control. Model predictive control systems have shown the ability to maintain biomass trajectories within 6 to 12% of target profiles, while machine learning-enhanced controls have improved protein production compared with historical averages.

This matters for food applications because consistency is critical. A dairy protein must perform the same way in cheese, yogurt, ice cream, and beverages across multiple batches. An egg protein must keep its foaming, gelling, and emulsification behavior. A heme or myoglobin ingredient must deliver stable color and flavor in meat analogues.

| Strategic Implication: |

| Teams should test early under pilot-relevant conditions, not only in shake flasks or small bioreactors. They should use scale-down models, real-time monitoring, and process control tools to understand how the strain behaves under industrial stress. |

Challenge 3: Downstream processing is the biggest cost barrier

Downstream processing is one of the clearest bottlenecks in precision fermentation. Conventional chromatography was built for high-value pharmaceutical proteins, not bulk food proteins. For alternative protein, this creates a major cost mismatch.

Purification can account for 50 to 80% of total production costs. For food applications, the goal is often functional purity rather than pharmaceutical-grade purity. The ingredient must deliver foaming, gelling, solubility, emulsification, flavor, or texture performance at a cost the market can accept.

Several lower-cost approaches are emerging. Solid PEG precipitation can reduce costs by 45 to 53% compared with Protein A chromatography. Aqueous two-phase systems, membrane filtration, coacervation, continuous downstream processing, and selective precipitation are also gaining attention. Many of these approaches still need stronger validation for food-grade, high-volume proteins.

| Strategic Implication: |

| Downstream processing should be designed alongside strain development. Teams should ask whether the protein can be secreted, whether chromatography can be avoided, what purity level is truly needed, and whether the recovery method preserves food functionality. |

Challenge 4: Feedstock cost will shape price parity

Fermentation economics depend heavily on feedstock. Refined glucose and sucrose are reliable, but they can be expensive and exposed to price volatility. They can also weaken the sustainability case if they depend on agricultural inputs that compete with food supply chains.

Purified sugars can represent 30 to 50% of production costs, making feedstock diversification a major opportunity. Alternative inputs include lignocellulosic residues, spent microbial biomass, agro-industrial side streams, C1 compounds, and biogas-linked streams.

C1 fermentation is especially important for long-term strategy. Methanol, methane, formate, CO₂-derived substrates, and hydrogen-based systems could reduce dependence on agricultural sugars. Hydrogen-oxidizing bacteria and methanol-based systems are gaining attention, but they still require careful assessment around safety, yield, energy use, process stability, and regulation.

| Strategic Implication: |

| Food companies should evaluate whether their own side streams from grain, dairy, brewing, sugar, fruit, vegetable, or oilseed processing can support fermentation. Each stream must be tested for consistency, impurities, microbial growth, downstream impact, and regulatory fit. |

Challenge 5: Food functionality is not guaranteed

Precision fermentation ingredients must work in real food systems. Producing the target molecule is only the starting point.

Dairy proteins need heat stability, acid stability, solubility, creaminess, melt, stretch, and gelation. Egg proteins need foaming, binding, emulsification, and heat-induced gelation. Meat-related proteins need to improve color, aroma, flavor, and texture in plant-based or hybrid systems.

The analysis shows dairy as the most mature application area, with whey and casein attracting the strongest activity. Egg proteins are emerging, led by ovalbumin. Meat applications are more focused on high-impact functional ingredients such as heme and myoglobin rather than bulk protein replacement.

The key issue is that “animal-identical” does not always mean “application-ready.” Processing conditions, glycosylation patterns, protein folding, and impurities can all affect performance.

| Strategic Implication: |

| Teams should test ingredients in target applications early. UHT beverages, acidic yogurts, frozen desserts, baked goods, cheese systems, and high-moisture extrusion can all expose problems that are invisible in isolated lab assays. |

Challenge 6: Consumer trial does not mean repeat purchase

Consumer interest is real, but adoption is not guaranteed. Across studies, 50 to 80% of consumers may be willing to try precision fermentation products, but only 17 to 35% are willing to buy them regularly. The gap is linked to concerns about naturalness, unfamiliar technology, GMO associations, and confusion around terms like “animal-free.”

Dairy appears to have a stronger starting point than some other categories. In a five-country survey cited in the analysis, 78.8% of consumers were likely to try animal-free dairy cheese, and 70.5% were likely to buy it. Still, taste remains a stronger purchase driver than environmental claims.

| Strategic Implication: |

| R&D teams should prioritize sensory quality and familiar formats. Cheese, yogurt, ice cream, protein beverages, bakery, and hybrid meat products may offer stronger adoption paths than unfamiliar product concepts. |

Challenge 7: Regulation varies sharply by market

Regulatory approval is uneven across regions. The U.S. GRAS pathway can offer timelines of around 6 to 12 months, while the EU Novel Food pathway can require 18 to 24 months and more extensive safety review. The EU also places greater scrutiny on genetically modified microorganism residues, residual DNA, and viable microbes in final ingredients.

Other markets, including India, Singapore, Israel, Australia, the UK, Switzerland, and South Korea, are developing or refining their own frameworks. This creates opportunities for staged market entry, but it also increases complexity for R&D planning.

Safety gaps remain important. Teams need data on cell line integrity, digestibility, allergenicity, nutritional impact, residual DNA, host cell proteins, endotoxins, and contamination control.

| Strategic Implication: |

| Regulatory strategy should guide host selection, genetic constructs, media design, purification choices, analytical methods, and labeling claims from the beginning. |

New Opportunities in Precision Fermentation

1. B2B ingredients can scale faster than finished consumer products

B2B ingredient markets are a strong opportunity because they reduce the burden of consumer education and focus on clear functional value. These include cultivated meat growth factors, collagen, functional enzymes, dairy proteins, heme proteins, flavor modulators, and processing aids.

For R&D teams, this means precision fermentation should not be viewed only as a path to animal-free milk, cheese, or eggs. It can also improve existing food systems by solving specific formulation problems.

2. Hybrid products offer a practical market entry route

Full replacement of animal proteins may take longer because of cost and functionality limits. Hybrid products can use small amounts of fermentation-derived ingredients to improve plant-based or conventional products.

This could include fermentation-derived casein for better cheese melt, egg proteins for bakery performance, myoglobin for meat analogue flavor, or enzymes that improve plant protein texture.

3. Downstream processing can become a competitive advantage

Since purification is one of the largest cost drivers, companies that develop lower-cost recovery methods can gain a strong position. Membrane filtration, selective precipitation, coacervation, and continuous processing are key areas to watch.

This is not just an operations issue. It can become a source of IP, margin protection, and speed-to-scale.

4. Circular feedstocks can improve both cost and sustainability

Spent microbial biomass, lignocellulosic residues, agro-industrial side streams, and biogas-linked inputs are underused. These feedstocks could reduce raw material costs and improve sustainability if they can support consistent production.

Large F&B companies may have an advantage because they already control or influence major side-stream networks.

5. Geographic expansion can unlock manufacturing advantages

Current food-focused fermentation capacity is concentrated in Europe and the U.S. Global capacity is about 16 million liters across 48 producers and 41 food-exclusive CMOs, with 47% in Europe and 34% in the U.S. This leaves gaps in regions such as Africa, Latin America, and Southeast Asia.

Regions with low-cost feedstocks, renewable energy, government incentives, and food security priorities could become important production hubs.

What R&D Teams Need to Do Next

1. Prioritize targets based on function

R&D teams should not select molecules only because they are technically interesting. They should prioritize ingredients that solve clear product problems, such as better melt in cheese, foam in egg alternatives, creaminess in dairy, flavor in meat analogues, or heat stability in protein beverages.

2. Build a host-product-process map

Each ingredient should be evaluated across three linked choices: the target protein, the microbial host, and the production process. A strong target with the wrong host or costly recovery process may fail commercially.

3. Run early techno-economic screening

Before deep development, teams should estimate titer requirements, feedstock cost, downstream cost, energy use, capex, and expected selling price. The shows that cost parity often depends on titers above 50 g/L, making early economic screening essential.

4. Treat downstream processing as a core R&D workstream

Purification must be designed alongside strain development. Teams should test whether the protein can be secreted, whether chromatography can be avoided, and whether food-grade recovery methods can preserve functionality.

5. Validate ingredients in real food systems

R&D teams should test performance in target applications early. Heat treatment, pH, freezing, extrusion, baking, drying, and storage can all change protein behavior.

6. Use partnerships to close capability gaps

Most F&B companies will need partners for strain engineering, fermentation scale-up, downstream processing, regulatory testing, and pilot manufacturing. This shows that the sector is already shifting toward B2B ingredient models, distributed manufacturing, and partnerships with CPG companies and infrastructure providers.

7. Design for regulatory approval from day one

Regulatory strategy should guide host selection, genetic constructs, media ingredients, purification methods, impurity testing, allergenicity assessment, and labeling claims.

How SLATE Helps R&D Teams Find the Right Precision Fermentation Opportunities

Precision fermentation is becoming harder to track because the important signals are spread across patents, research papers, startups, regulatory updates, scale-up activity, and ingredient launches. For R&D teams, the challenge is not finding information. It is knowing which developments matter, which ones are technically mature, and which ones can support real product decisions.

SLATE helps R&D teams turn this scattered information into a clear innovation roadmap. It can track emerging research clusters, identify where patent activity is rising, compare technologies across strain engineering, feedstock use, downstream processing, and process control, and highlight gaps where competitors have not yet built strong positions.

In precision fermentation, this means SLATE can help teams answer practical questions:

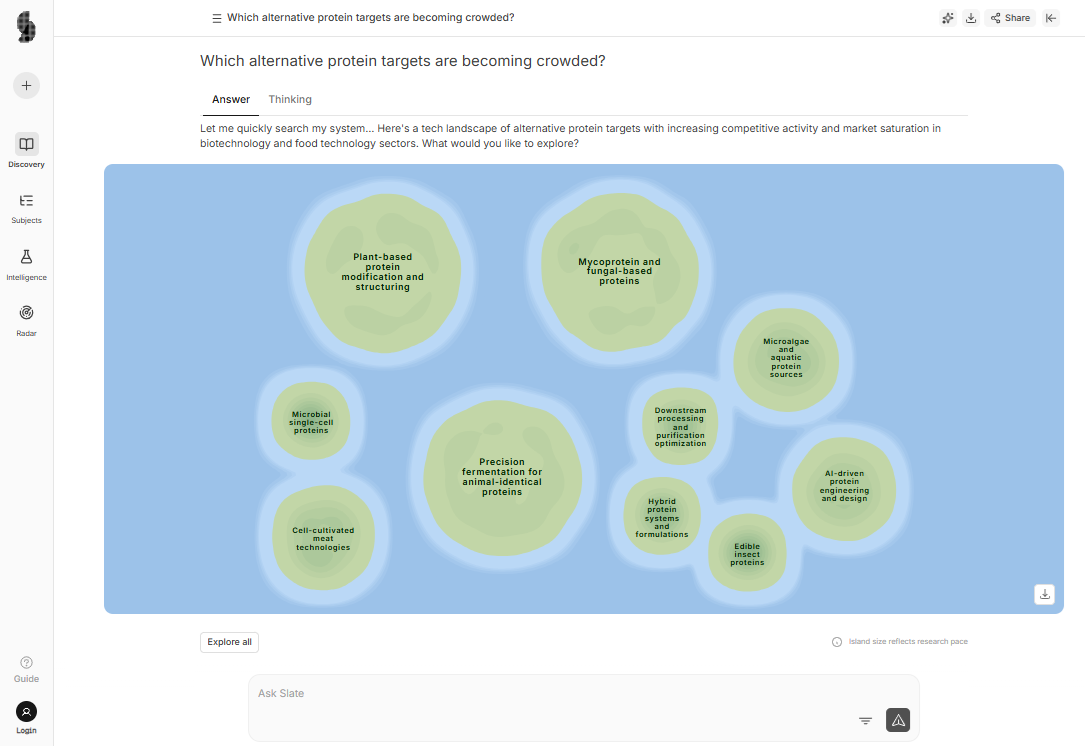

- Which alternative protein targets are becoming crowded?

- Which host organisms and strain systems are gaining traction?

- Where are companies solving scale-up and cost bottlenecks?

- Which technologies are still early but worth monitoring?

- Which startups, suppliers, or research groups are relevant for partnership?

- Where should the company build, partner, invest, or wait?

Strain engineering and process control together account for nearly half of recent precision fermentation innovation, while downstream processing remains under-addressed despite being a major cost driver. SLATE can help R&D teams monitor these shifts continuously, so they are not reacting after a market moves.

For a large F&B company, SLATE becomes a decision-support layer. It helps teams move from trend tracking to action: selecting the right molecules, identifying technical risks early, finding partnership opportunities, and building a stronger alternative protein pipeline with better evidence behind each decision.